SFRS(I)18 Presentation And Disclosure In Financial Statements

What You Need to Know (Part 1):

Main Business Activity related to investing in assets (SMBA 1) and the interplay with the investing category

Foreword

by Lim Ju May, Director, Assurance and Technical Accounting at CLA Global TS

I wrote an article “NEW IFRS 18 ‘Presentation and Disclosure in Financial Statements’ Replaces IAS 1 ‘Presentation of Financial Statements’ – An overview of what is new and how it will improve financial reporting” in October 2024. In that piece, I provided an overview of what is new in IFRS 18, the new concepts and how these concepts work to improve financial reporting. I highlighted the following three new concepts:

- Cookie-cutter Statement of Profit or Loss;

- Management-defined performance measures (“MPMs”); and

- Enhanced requirements for grouping (aggregation and disaggregation)

of information.

In this inaugural piece of What You Need To Know series, I will expound on the topic of Main Business Activity (“MBA”).

Specified Main Business activity (“SMBA”)

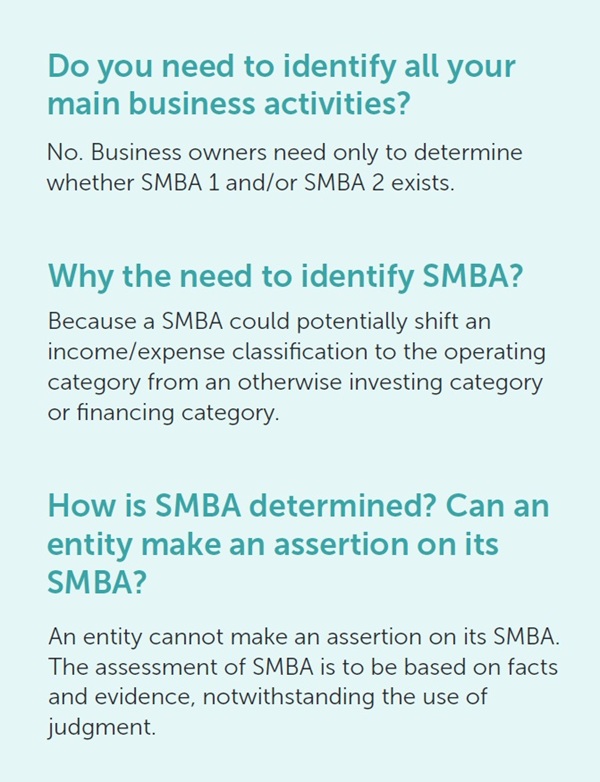

SFRS(I) 18 weaves the concept of ‘Specified Main Business Activity’ into the classification rules of income and expenses. As a business owner, you will need to understand your main business activities at the reporting entity level. More specifically, whether your reporting entity invests in assets or provides financing to customers.

SMBA 1 – Investing in particular types of assets

SFRS(I) 18 requires an entity to assess whether it has a SMBA 1 and to disclose the fact if it has. Before we proceed, I should state at the outset that the SMBA 1 assessment is not easy. Hence the four key steps below to help you navigate this.

STEP 1: Separate out what’s not assets under SMBA 1

To pin down SMBA 1, lets separate out the particular types of assets that could fall under SMBA 1. We do this by first identifying the assets that will never fall under SMBA 1.

What assets will never fall under SMBA 1?

Operating Assets

Income and expenses from operating assets will always fall under the operating category – hence never under SMBA 1.

What are operating assets?

These are assets that do not generate a return individually and largely independently of the entity’s other resources. The opposite of other assets under paragraph 53(c) of SFRS(I) 18.

What are examples of operating assets?

Trade receivables, property, plant and equipment.

Investments in associates, joint ventures and unconsolidated entities accounted for under the equity method

Income and expenses from the above investments will always fall under the investing category – never under the operating category.

STEP 2: Decide on Cash and cash equivalents

Are cash and cash equivalents (“C&CE”) operating assets? Some entities do hold C&CE for operational purposes as part of working capital. IASB acknowledged that some entities hold cash for operational purposes – for example, as part of working capital. These C&CE should qualify as operating assets if they hold large amount of C&CE for operational purposes.

However, before jumping to the conclusion that interest income from C&CE are classified under the operating category, please read the rest of this article.

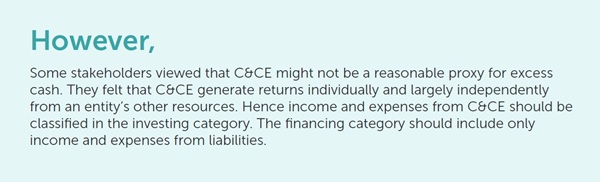

For some entities, C&CE are excess cash and temporary investments of excess cash. By excess cash, it goes without saying that these are not operating assets.

The IASB first considered requiring an entity to classify income and expenses form excess cash (and temporary investments of excess cash) in the financing category because entities typically treat excess cash as part of their financing.

How excess cash is managed is interrelated with decisions about debt and equity financing. IASB felt that C&CE as defined in ISA 7 “Statement of Cash Flows” could be used as a proxy to excess cash.

IASB conceded and concluded that income and expenses from C&CE are to be classified in the investing category of the income statement unless it falls under SMBA 1.

Can an entity say that it invests in C&CE as a MBA and hence operating category classification?

The answer is it depends. One cannot outright assert that it invests in C&CE as a MBA. As elaborated in the above paragraphs, IASB had put in much thought into how an entity classifies income and expenses from C&CE. How then will income and expenses from C&CE qualify for classification in the operating category of the Income Statement?

To answer this, please see paragraph 56 of SFRS(I) 18. Here, IASB provided an exemption for classifying the income and expenses from C&CE in the operating category instead of the required investing category.

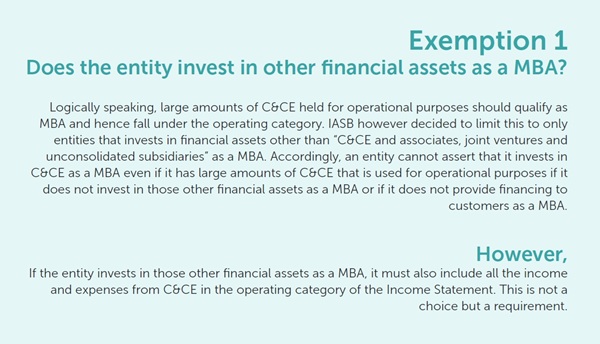

STEP 3: Investments in associates, joint ventures and unconsolidated subsidiaries not accounted for under the equity method

This step is straightforward.

Does the entity invest in the above as a MBA? If the answer is yes – it is SMBA 1 and the income and expenses from these investments

are to be classified under the operating category instead of the investing category in the Income Statement.

If the entity does not invest in the above assets as a MBA, SMBA 1 does not apply and the investing category classification remains.

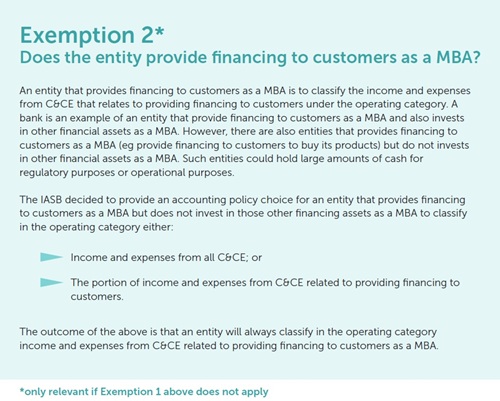

Step 4: Other non-operating assets (other than C&CE and investments in associates, joint ventures and unconsolidated subsidiaries)

When it comes to accounting standards, definition is everything.

The above category of non-operating assets applies to those assets that generate a return individually and largely independently of the

entity’s other resources. Examples are debt or equity investments and investments in properties, and receivables for rent generated by those properties.

Does the entity invest in the above as a MBA? If the answer is yes – it is SMBA 1 and the income and expenses from these investments are to be classified under the operating category instead of the investing category in the Income Statement.

If the entity does not invest in the above assets as a MBA, SMBA 1 does not apply and the investing category classification remains.

Closing Remarks

Discerning the interplay between SMBA 1 and the investing category is the first step towards developing your cookie-cutter statement of profit or loss.

Stay in tune to Part 2.

View the full article in PDF here.

Article by

Lim Ju May

Director, Assurance and Technical Accounting

CLA Global TS