SFRS(I)18 Presentation And Disclosure In Financial Statements

What You Need to Know (Part 2):

The Financing Category whereby an entity does not provide financing to customers as a main business activity

Foreword

by Lim Ju May, Director, Assurance and Technical Accounting at CLA Global TS

I wrote this series’ inaugural piece “What You Need to Know [Part 1] – Main Business Activity related to investing in assets (SMBA 1) and the interplay with the investing category” last year. In that piece, I introduced the concept of Main Business Activity (“MBA”) vis-a-vis the classification rules of income and expenses. I delved into investing in particular types of assets and provided the following four key steps to assist in determining whether an entity has SMBA 1:

- Step 1: Separate out what’s not assets under SMBA 1;

- Step 2: Decide on Cash and Cash Equivalents;

- Step 3: Investments in associates, joint ventures and unconsolidated subsidiaries not accounted for under the equity method; and

- Step 4: Other non-operating assets (other than C&CE and investments in associates, joint ventures and unconsolidated subsidiaries).

In this second piece of the ‘What You Need To Know’ series, we will delve into the financing category of the statement of profit or loss.

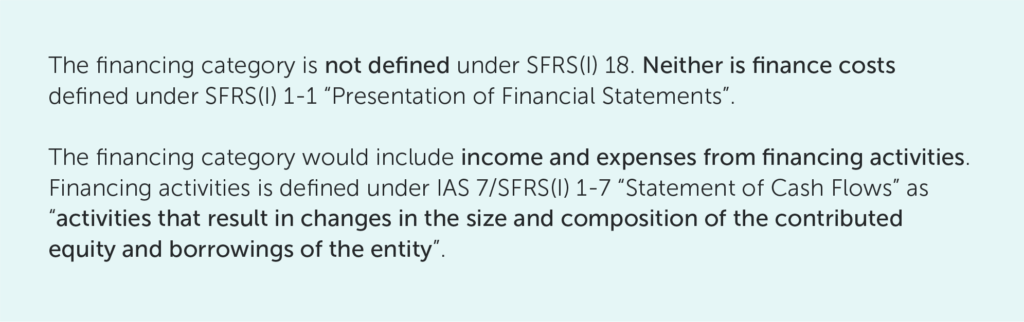

The Financing Category

SFRS(I) 18 requires all income and expenses to be to be classified under one of five categories. This cookie-cutter statement of profit or loss includes three new categories – investing category, financing category and operating category. The other two categories are the income tax category and the discontinued operations category.

SFRS(I) 18 also requires entities to present two new defined subtotals in the statement of profit or loss – operating profit; and profit before financing and income taxes (which comprises operating profit and income/expenses under the investing category).

Because this definition of ‘financing activities’ under IAS 7 is difficult to apply, the IASB considered amending IAS 7 to clarify the definition of ‘financing activities’ so that it can be applied consistently.

However, due to the challenges in developing a new definition for ‘financing activities’, the IASB decided not to amend the definition of ‘financing activities’ under IAS 7.

Instead, the IASB developed a practical approach that focused more broadly on income and expenses that are financing by nature.

So what is this practical approach?

Please read on further…

This is the practical approach developed by IASB that focuses more broadly on income and expenses that are financing in nature. IASB’s end goal is that regardless of whether a liability is considered part of an entity’s financing activities, income and expenses that are financing by nature will be classified in the financing category.

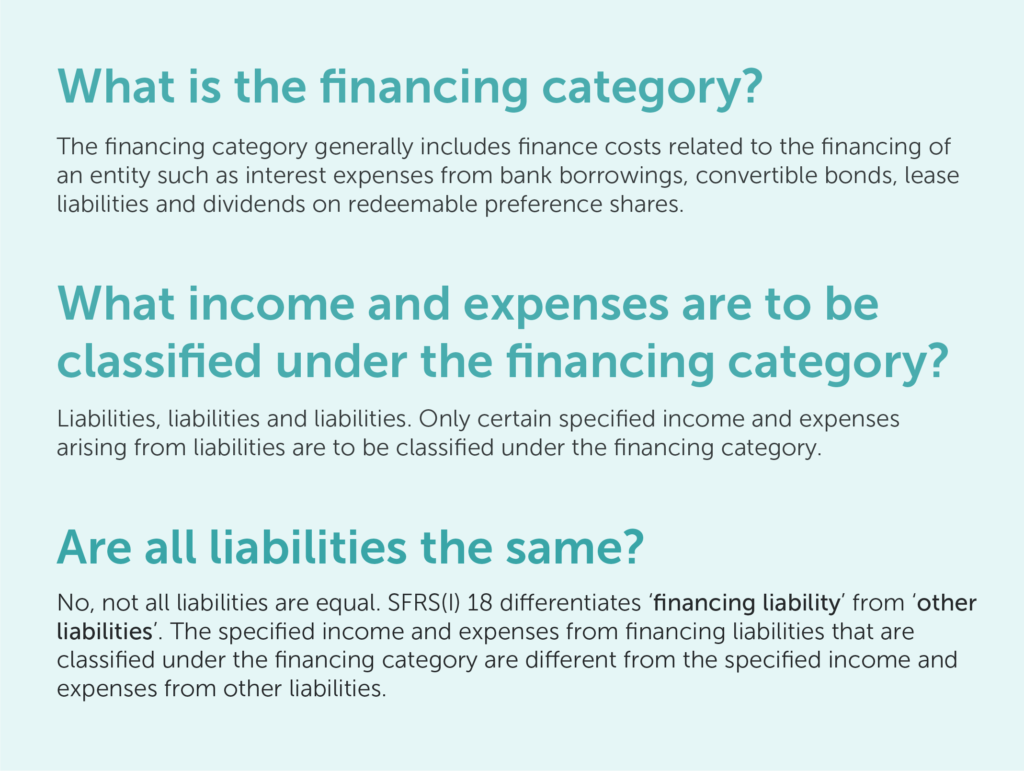

Financial Liabilities

What are financing liabilities?

Financing liabilities are liabilities that arise from transactions that involve only the raising of finance.

What are examples of financing liabilities?

- A debt instrument that will be settled in cash such as loans and bonds;

- A liability under a supplier financing arrangement;

- A bond that will be settled through delivery of an entity’s shares; and

- An obligation for an entity to purchase its own equity instruments.

What are the specified income and expenses from financing liabilities to be classified in the financing category?

Income and expenses from initial and subsequent measurement of liabilities, including derecognition of liabilities. Examples are:

- Interest expenses (for e.g. on debt instruments issued);

- Fair value gains and losses (for e.g. a liability designated at fair value through profit or loss);

- Dividends on issued shares classified as liabilities; and

- Income and expenses from the derecognition of liability.

The incremental expenses directly attributable to the issue and extinguishment of the liabilities – for e.g., transaction costs.

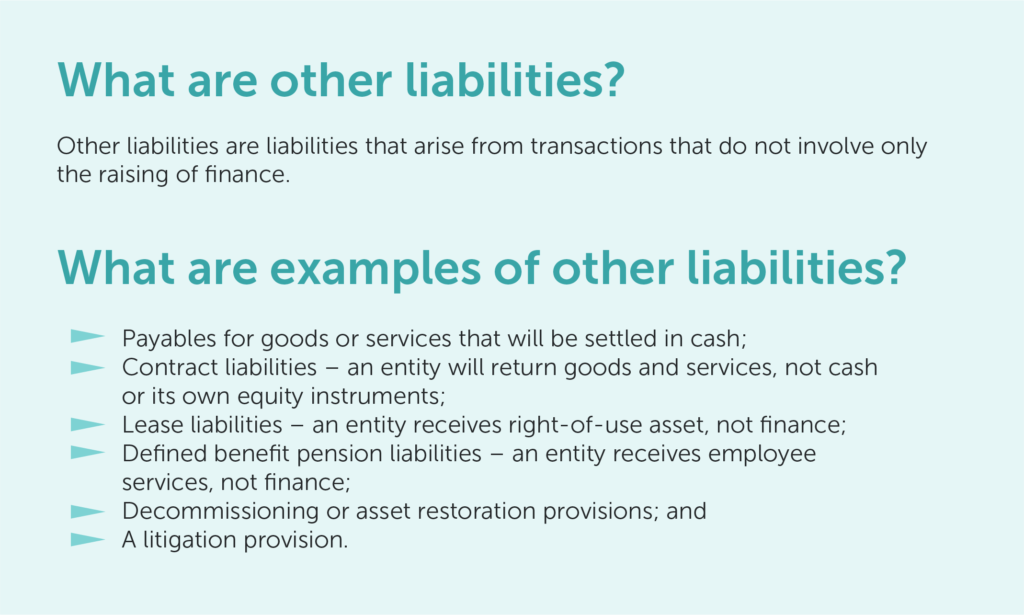

Other Liabilities

Under ‘other liabilities’, only interest income and expenses arising from these ‘other liabilities’ are to be classified in the financing category.

What are the specified income and expenses from other liabilities to be classified in the financing category?

Interest income and expenses. Examples are:

- Interest expenses on payables arising from purchase of goods or services, applying SFRS(I) 9;

- Interest expenses on a contract liability with a significant financing component as specified under SFRS(I) 15;

- Interest expenses on a lease liability, applying SFRS(I) 16;

- Net interest expense (income) on a net defined benefit liability (asset), applying SFRS(I) 19; and

- The increase in the discounted amount of a provision arising from the passage of time and the effect of any change in the discount rate on the provisions, applying SFRS(I) 37.

Income and expenses arising from changes in interest rates.

Closing Remarks

I have dedicated Part 2 of the What You Need To Know series to understanding the fundamentals of the financing category. This will pave the way to Part 3 whereby we will examine the main business activity of providing finance to customers and its interplay with the financing category.

Stay in tune to Part 3.

View the full article in PDF here.

Article by

Lim Ju May

Director, Assurance and Technical Accounting

CLA Global TS