Article by Lim Ju May, Director, Assurance and Technical at CLA Global TS.

NEW IFRS 18 Presentation and Disclosure in Financial Statements Replaces IAS 1 Presentation of Financial Statements – An overview of what is new and how it will improve financial reporting

Important milestone for communication of financial performance

The issuance of IFRS 18 Presentation and Disclosure in Financial Statements on 9 April 2024 marks a significant milestone in the communication of financial performance by companies. Its equivalent in Singapore, SFRS(I) 18 and FRS 118 were recently issued by the Accounting Standards Committee on 4 October 2024.

Effective date and first-time application

IFRS 18 is effective from 1 January 2027 with early application permitted.

It requires retrospective application which means that the comparative information for the preceding period in the first year or period of application needs to be restated. Listed entities announcing condensed financial statements for the first interim period applying IFRS 18 will need to be prepared earlier to ensure that the comparatives for the 6 months to 30 June 2027 (or 3 months to 31 March 2027) condensed financial statements are available.

IFRS 18 will not affect how companies measure financial performance but will affect how companies present and disclose financial performance. Consequently, the first-time application of IFRS 18 will not result in any adjustments to the opening retained earnings.

Companies however will need to disclose for the immediately preceding comparative period, a reconciliation for each line item in the statement of profit or loss between:

- the restated amounts presented applying IFRS 18; and

- the amount previously presented applying IAS 1.

What is new in IFRS 18 and how will it improve financial reporting?

The diagram above provides a pictorial overview of how the key concepts in IFRS 18 interconnects to improve financial reporting. What are these key concepts? Generally the new changes can be categorised under three key concepts.

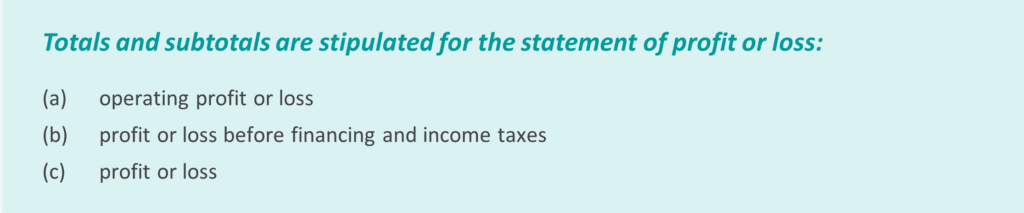

The first is the crux or most important aspect of IFRS 18, without which IFRS 18 would very likely not exist. It is the new requirement for the statement of profit or loss, as shown in the left column of the diagram, and further elaborated under the section “Cookie-Cutter Statement of Profit or Loss”.

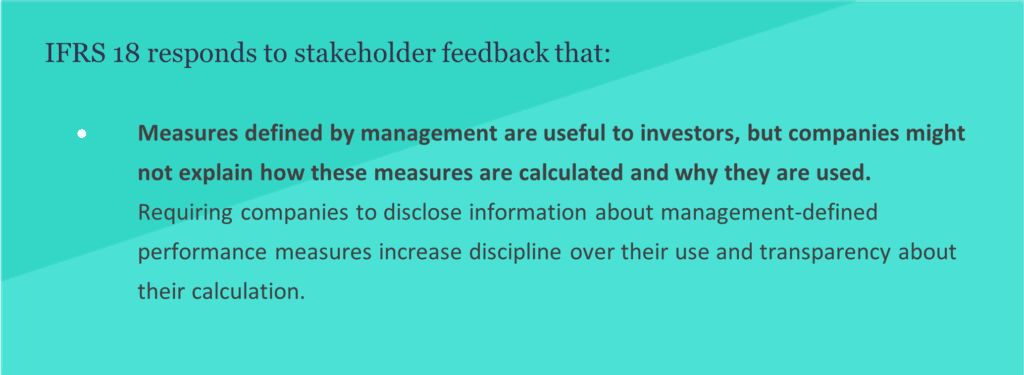

Management-defined performance measures (“MPMs”)

The second key concept is the requirement for the disclosures about MPMs in the notes to the financial statements. This requirement connects the dots between non-GAAP measures used by management to communicate an entity’s financial performance as a whole and IFRS-specified subtotals of income and expenses. Non-GAAP measures are measures that are not defined by IFRS Accounting Standards. IFRS 18 details what constitutes MPMs and their disclosure requirements. Do note that entities that do not make public communications outside financial statements about its financial performance as a whole will not have any MPMs.

Cookie-Cutter Statement of Profit or Loss

A gingerbread man cookie-cutter is how I visualise the new Statements of Profits or Losses from year 2027 onwards.

- Gingerbread man’s torso – Income and expenses from operations

- Gingerbread man’s right hand – Investment income

- Gingerbread man’s left hand – Financing expenses

- Gingerbread man’s head – Income taxes

- Gingerbread man’s legs – Discontinued operations

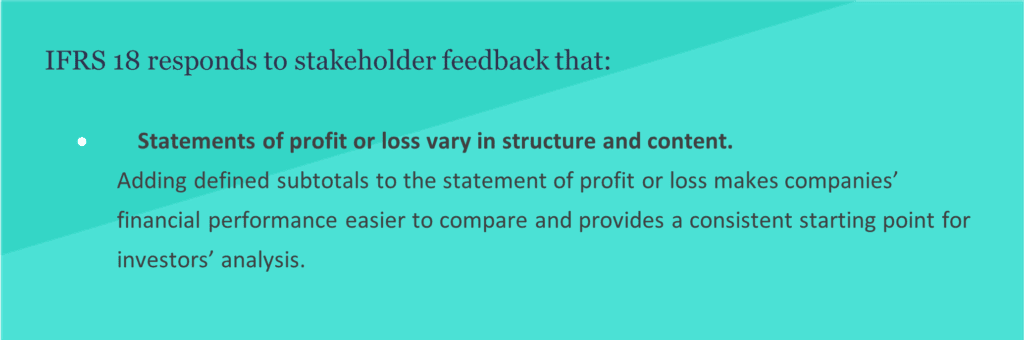

With a cookie-cutter for the statement of profit or loss, all entities will have a pre-set similar structure for their income statements. This provides a consistent structured summary of an entity’s income and expenses, thereby facilitating the communication of an entity’s financial performance and addressing stakeholder feedback.

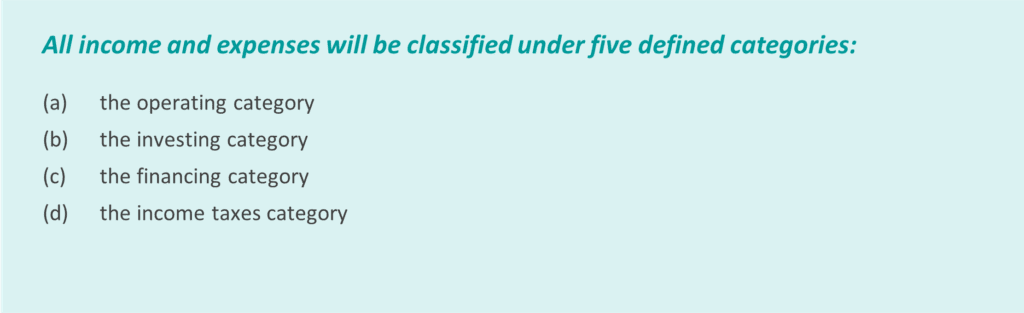

Three new categories in the statement of profit or loss

IFRS 18 requires three new defined categories – investing; financing; and operating. This together with the two new required subtotals will provide a consistent structure of the statement of profit or loss i.e. a cookie-cutter statement of profit or loss.

Investing – Financing – Operating are not new categories and many companies do have such categories in their income statement. However, because IAS 1 does not define these categories, there is diversity in practice as to what constitutes financing or investing or operating.

- Entities that classify dividends/interests from investments in shares, bonds or fixed deposits under the “other income” category will under IFRS 18 be required to classify them under the investing category.

- If previously one classifies depreciation/impairment of investment property expenses under the operating category, it is no longer allowed. Instead, these expenses must be classified under the investing category.

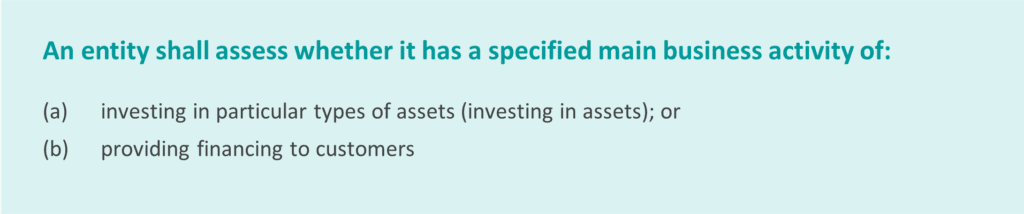

How about investment entities, insurers or investment property companies? Where should the income/expenses from investments in the shares of entities which are associates, joint ventures and subsidiaries be classified? Should the dividends be classified under the investing category or the operating category? How about the share of profit of associates or joint ventures when applying the equity method?

IFRS 18 introduces the above concept of “specified main business activities”, whereby an entity with a specified main business activity classifies in the operating category some income and expenses that would have been classified in the investing or financing category if the activity were not a main business activity.

Needless to say, IFRS 18 has detailed requirements on categorizations both in its main body and in its application guidance. I will endeavour to unravel the maze of accounting rules surrounding what gets classified into each of the categories in my next article.

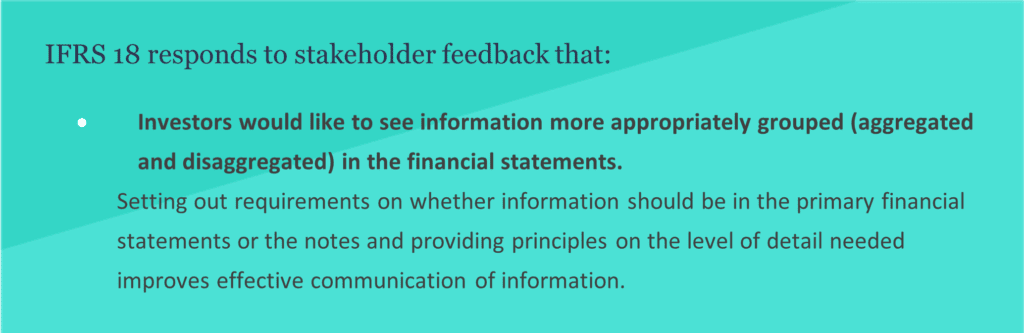

Enhanced requirements for grouping (aggregation and disaggregation) of information

The third and final key concept comprises a number of inter-related individual concepts that work together to anchor financial reporting towards better communication in financial statements. More specifically the determination of line items to be included in the Primary Financial statements and the depth of disclosures in the notes to the financial statements.

These concepts in IFRS 18 comprises:

- Objective of financial statements

- Roles of primary financial statements and the notes

- Principles of aggregation and disaggregation of information

- Ensure that aggregation & disaggregation do not obscure material information

This is an area that is complex and requires the exercise of judgment. It is at its current state, theoretical and conceptual but I have no doubt that future amendments will make refinements for pragmatic application.

Closing Remarks

I trust that the NEW in IFRS 18 is the start of a journey towards better communication of an entity’s financial performance. With the introduction of two new defined sub-totals and specifications on how to classify items into the different categories in the statement of profit or loss, entities will be able to better communicate performance reporting via the statement of profit or loss and this would lead to improved comparability.

View the full article in PDF here.

Article by:

Lim Ju May

Director, Assurance and Technical Accounting

CLA Global TS

For more information, please contact us.