An overview of Singapore’s Global Minimum Tax (Pillar Two), including MTT and DTT

scope, timelines, and key considerations for multinational groups

Global Minimum Tax (Pillar Two): Are You Likely to Be in Scope in Singapore?

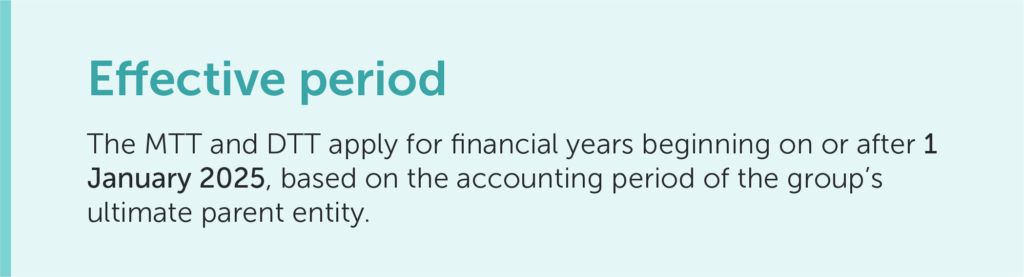

Singapore has implemented the Global Minimum Tax under Pillar Two through the Minimum Top-up Tax (MTT) and Domestic Top-up Tax (DTT) framework, effective for financial years beginning on or after 1 January 2025.

While the rules apply only to groups above a specified size, they introduce new concepts, calculations, and reporting obligations that differ materially from Singapore’s existing corporate income tax regime. As a result, many groups with operations in Singapore are now assessing whether—and how—the rules may affect them.

This article provides a high-level overview to help groups quickly determine whether a Pillar Two assessment may be required, and where further analysis is typically needed.

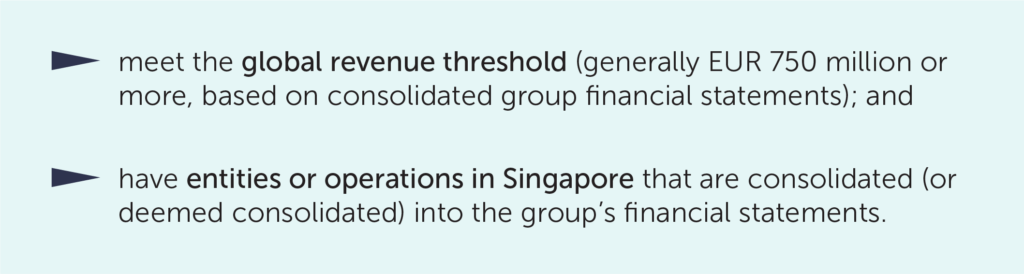

At a Glance: Who Is Potentially in Scope?

At a high level, Singapore’s MTT and DTT apply to multinational enterprise (MNE) groups that:

Even where these conditions are met, exclusions, transitional reliefs, and safe harbours may significantly reduce or eliminate top-up tax exposure—although compliance and reporting obligations may still arise.

Key Considerations for Singapore Entities

In practice, determining Pillar Two exposure is rarely a simple “yes or no” exercise. Common questions we see include:

- whether a Singapore entity is within scope based on group consolidation rules;

- whether the group qualifies for transitional or permanent safe harbours;

- whether Singapore’s DTT or MTT may apply, even if the group parent is located overseas; and

- what data, filing, and coordination obligations arise at the Singapore entity level, regardless of whether top-up tax is ultimately payable.

These questions often require coordination between local finance teams and group-level tax or reporting functions.

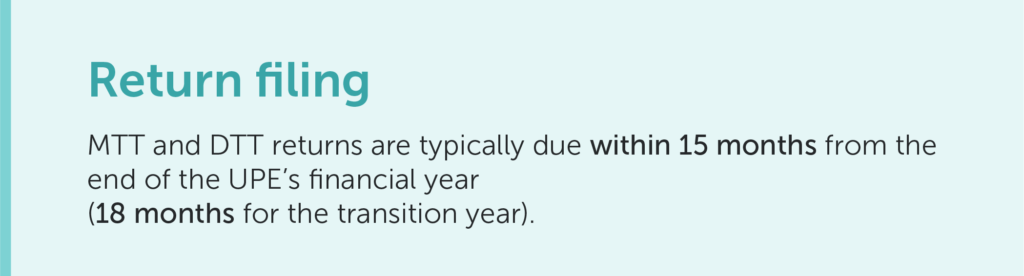

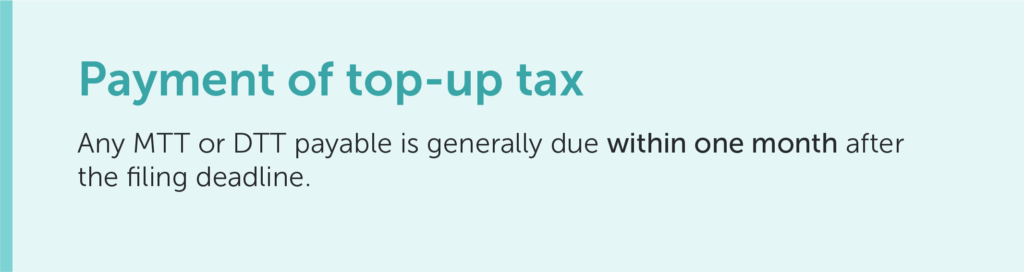

Key Pillar Two Timelines (Singapore)

For groups within scope, Singapore’s MTT and DTT introduce new registration, filing, and payment timelines that do not align neatly with the traditional corporate income tax cycle.

At a high level:

These timelines are indicative and may vary depending on group-specific facts, including transition status and designation of filing entities.

Our Services: How We Support Companies under Singapore’s Global Minimum Tax

We support companies in navigating Singapore’s Pillar Two regime through the following services:

- Assessing whether the group and Singapore entity are within scope

We determine whether the Singapore entity belongs to an MNE group subject to the MTT or DTT, assess whether it qualifies as an excluded or exempt entity, and evaluate the availability of transitional or permanent safe harbours. - Identifying and gathering Pillar Two data

We assist in identifying and compiling the data required to comply with Pillar Two obligations and help clarify the responsibilities of the Singapore entity within the wider group. - Establishing the Pillar Two tax base

We analyse adjusted financial accounting income in accordance with Singapore’s MTT and DTT rules and identify relevant adjustments, exclusions, and simplifications. - Supporting the determination of any top-up tax payable

Based on the data and analysis performed, we assist in determining whether any top-up tax arises under the DTT or MTT and support the related computations. - Assessing risks and areas of uncertainty

We help identify interpretational or compliance risk areas and provide practical observations tailored to the group’s structure and Singapore operations. - Pillar Two reporting and ongoing compliance

As reporting requirements are finalised, we support the preparation or review of relevant filings and help ensure consistency with group-level Pillar Two positions.

Why Early Assessment Matters

Even where no top-up tax is ultimately payable, many groups find that early assessment helps to:

- identify data gaps—where information required for Pillar Two is unavailable, incomplete, or not readily aligned with group reporting requirements—well ahead of filing deadlines;

- align Singapore positions with group-level Pillar Two reporting, particularly where timelines and responsibilities differ across jurisdictions; and

- avoid last-minute complexity around entity designation, reporting timelines, and filing obligations.

How We Can Help

If your group has operations in Singapore and may fall within scope of Pillar Two, an initial assessment can help clarify obligations and avoid unnecessary complexity later.

Please contact us to discuss how Singapore’s Global Minimum Tax rules may apply to your group and how we can support you.

This article is indicative only. Scope and obligations depend on group-specific facts.

View the full article in PDF here.

CONTACT US

CLA Global TS Business Advisors

Tax Advisory Specialists

|

Edwin Leow Co-Advisory Leader Director, Head of Tax edwinleow@sg.cla-ts.com |

|

Jason Oon Associate Director, Tax jasonoon@sg.cla-ts.com |