1. Estimated Chargeable Income (“ECI”)

According to Section 63(1) of the Singapore Income Tax Act (“SITA”), every person (including a company) not being an individual or a Hindu joint family who has not filed a tax return for any year of assessment (“YA”), is required to furnish an estimate of his chargeable income and revenue to the Inland Revenue Authority of Singapore (“IRAS”) within 3 months after the end of the accounting period relating to that YA.

For taxation purposes, a company includes a business entity incorporated or registered under the Singapore Companies Act or a foreign company registered in Singapore such as a branch of a foreign company or a foreign company incorporated or registered outside Singapore.

Unless the waiver to file the ECI is applicable, if the ECI is not filed by the statutory deadline, the IRAS may issue a Notice of Assessment (“NOA”) based on its own estimate of the person’s chargeable income. The IRAS’ estimated assessment may be excessive, and if the person does not agree to the estimated assessment, an objection to the NOA must be lodged within two months of the date of the NOA. Otherwise, the IRAS has the right to treat the estimated assessment as a final assessment and refuse amendment of the estimated assessment even if the actual chargeable income is subsequently determined to be less than the ECI.

The ECI should be arrived at with reasonable accuracy. The ECI should be the amount before deducting the exempt amount under the partial tax exemption scheme or the tax exemption scheme for new start-up companies. If the ECI filed with the IRAS has been significantly underestimated, a revised ECI may be filed before the submission of the income tax return. Otherwise, the IRAS may require the Company to provide the reason for the significant understatement of the ECI.

Please inform us if the Company qualifies for the waiver to file the ECI. If otherwise, please furnish to us the Company’s ECI and gross revenue (i.e., the main income source) as soon as practicable before the filing deadline.

E-filing of the ECI has been made compulsory with effect from YA 2020. To enable our firm to e-file the ECI, the Company’s CorpPass Administrator has to authorise our firm to act as the Company’s tax agent at the CorpPass website at https://www.corppass.gov.sg. If the Company requires our assistance or information regarding the e-authorisation procedure, please let us know.

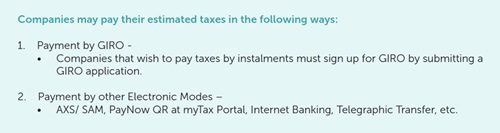

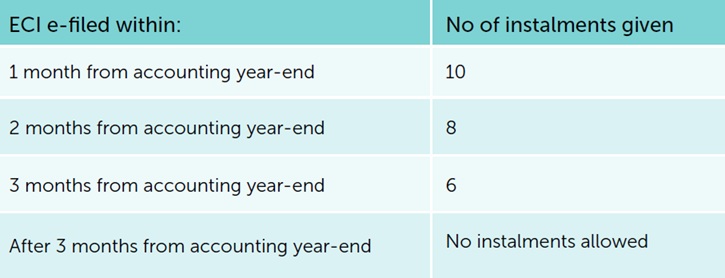

Only companies registered in Singapore that are on GIRO qualify for instalment payment. The table below summarises the number of instalments that can be allowed:

Companies are required to e-file the ECI by the 26th of each qualifying month to enjoy the maximum number of instalments allowable for that month.

The GIRO deduction date is every 6th of the month. Depending on the date of e-filing of the ECI, the first two instalments may be combined and deducted on the first GIRO deduction date.

2. Income Tax Return (Form C / C-S / C-S (Lite))

From YA 2020, all companies have been required to e-file their income tax returns. For YA 2026, all companies will be required to e-file their income tax returns by the statutory filing deadline of 30 November 2026.

Companies which satisfy certain conditions are given the option to e-file a simplified Form C (i.e., Form C-S or Form C-S (Lite)) with the IRAS for statutory tax submission purposes. The Company’s financial statements and income tax computation are not required to be submitted with the Form C-S or Form C-S

(Lite) but should be prepared and available for submission to the IRAS upon request (e.g. due to tax queries, audits, etc.). The income tax computation should be prepared as the Form C-S or Form C-S (Lite) is to be completed based on the income tax computation.

To meet the filing deadline, the Company should ensure that any information required for the preparation of the income tax return and income tax computation is furnished to us within our requested timeline in a complete and accurate manner. We regret to inform you that our firm cannot be held responsible if the requisite information is not provided on time resulting in a late submission of the income tax return. We should also emphasize that late filing penalties may be imposed and/or other enforcement actions may be taken by the IRAS if the income tax return is not submitted by the filing deadline.

In preparing the income tax return and income tax computation, a position may have to be taken with respect to the deductibility of an expense or chargeability of an income, and the extent of information to be disclosed. The position taken will be explained and discussed with the Company so that it can decide on the appropriate tax treatment.

If the Company is dormant (i.e., one that does not carry on business and has no income for the whole of the preceding year) and is expected to remain dormant for the next few years, it can apply to the IRAS for a waiver to submit the income tax return.

If the application is approved, the Company will not be issued the income tax return in future. However, if the Company commences/ re-commences business

or starts to receive any income, it is required to notify the IRAS in writing within one month from the date of commencement of business or the date it earned or received the income.

3. Multinational Enterprise Top-up Tax (“MTT”) and Domestic Top-up Tax (“DTT”)

Registration for MTT and DTT

Under the Multinational Enterprise (Minimum Tax) Act (“MMT Act”), all in-scope multinational enterprise (“MNE”) groups are required to register for MTT, DTT, and the filing of the GloBE Information Return (“GIR”). The registration process will begin in May 2026.

An MNE group is required to be registered under the MMT Act if all the following conditions are met:

- The MNE group has annual revenue of €750 million or more, as reported in the consolidated financial statements of the Ultimate Parent Entity (“UPE”) for at least two out of the four preceding financial years; and

- The MNE group has at least one Constituent Entity (“CE”) or a Joint Venture located in Singapore, or at least one Reverse Hybrid Entity that is incorporated or registered in Singapore.

The UPE of an MNE group must notify the Comptroller of Income Tax by submitting the group’s information through an online registration form.

- The registration form must be submitted within 6 months after the end of the group’s first financial year to which the MMT Act applies.

- If the UPE wishes to appoint a representative to register the MNE group on its behalf, the representative may be either a CE of the MNE group located in Singapore or a local tax agent.

A 10% surcharge on DTT and MTT (if applicable) may be imposed if an in-scope MNE group fails to notify the Comptroller of its registration liability under the MMT Act.

Filing of MTT/DTT returns and GIR/GIR notification filing

All registered MNE groups liable for the MTT and / or DTT are required to file tax returns on their top-up tax liability in Singapore. All registered MNE groups are also required to file a GIR with Singapore, unless the GIR is filed with another jurisdiction and, in such a case, a GIR notification (if Singapore will receive the GIR through a filing made in another jurisdiction via exchange of information) must be filed with Singapore.

The filing deadline is 15 months (or 18 months if it is the transition year) from the UPE’s financial year end.

Please reach out to us if the Company requires any assistance on the above matters.

4. Related Party Transactions

In Singapore, all related party transactions (“RPTs”) must be carried out on an arm’s length basis. Relevant provisions have been enacted in the SITA requiring arm’s length pricing for RPTs, and the IRAS has issued detailed transfer pricing (“TP”) guidelines. Singapore has also introduced Country-by-Country (“CbC”) reporting and RPT reporting.

Singapore Income Tax Act

Section 34D of the SITA stipulates the requirement for arm’s length pricing. The arm’s length principle requires that a transaction with a related party should be made under comparable conditions and circumstances as a transaction with an independent party. The premise is that where market forces drive the terms and conditions agreed in an independent party transaction, the pricing would reflect the true economic value of the contributions made by each party in that transaction.

Section 34D allows the IRAS to make the following TP adjustments:

- Increase the amount of income of the taxpayer that is accrued in or is derived in Singapore, or is received in Singapore from outside Singapore, had arm’s length conditions been applied.

- Reduce the deductions claimed by the taxpayer had arm’s length conditions been applied.

- Reduce the losses claimed by the taxpayer had arm’s length conditions been applied.

Section 34D also empowers the IRAS to disregard a transaction and, if appropriate, replace it with an alternative transaction. It has been clarified that the IRAS would generally avoid disregarding the form of the actual commercial or financial arrangement between related parties unless the form does not reflect the actual conduct or economic substance of the transaction.

Section 34E introduced with effect from YA 2019, a surcharge of 5% on the TP adjustment made under Section 34D, regardless of whether the taxpayer is in a taxable position after the TP adjustment.

Section 34F requires a company, the person making the return for a firm (including a partnership) or the trustee of a trust to prepare contemporaneous TP documentation with effect from YA 2019 in the following situations:

- The gross revenue from the trade or business of the company, firm or trust in the basis period for a year of assessment exceeds S$10 million and its related party transactions in the basis period are not exempted from the preparation of contemporaneous TP documentation.

- The company, firm or trustee of the trust was required to prepare TP documentation for a transaction in the previous basis period and its related party transactions in the current basis period are not exempted from the preparation of contemporaneous TP documentation.

Contemporaneous TP refers to documentation and information that taxpayers have relied upon to determine the transfer price prior to or at the time of undertaking the transactions.

The subsidiary legislation of the SITA provides for the exemption from the preparation of contemporaneous TP documentation in the following situations:

- Where the taxpayer transacts with a related party in Singapore and such local transactions (excluding related party loans) are subject to the same Singapore tax rates or exempt from Singapore tax for both parties:

- Where a related party domestic loan is provided between the taxpayer and a related party in Singapore prior to 1 January 2025 and the lender is not in the business of borrowing and lending money;

- Where a related party domestic loan of any amount is provided between the taxpayer and a related party in Singapore on or after 1 January 2025 where neither the lender nor the borrower is in the business of borrowing and lending money and the indicative margin is applied in accordance with the IRAS’ administrative practice;

- Where the taxpayer applies the indicative margin for a related party loan not exceeding S$15 million in accordance with the IRAS’ administrative practice;

- Where the taxpayer applies the 5% cost mark-up for certain routine support services;

- Where the RPT is covered by an agreement under an Advance Pricing Arrangement (“APA”). In such a situation, the taxpayer will keep relevant documents for the purpose of preparing the annual APA compliance report to demonstrate compliance with the terms of the agreement and the critical assumptions remain valid; or

- Where the RPT comes within a category of transactions under the first column of the table below and the total value of the RPTs in that category in the basis period [excluding the value or amount in sub-paragraphs (a) to (f)] does not exceed the value for that category set out in the second column of the table below:

![]()

¹The threshold per financial year for these categories of related party transactions has been increased from S$1 million to S$2 million with effect from YA 2026.

TP documentation, where required, has to be prepared no later than the statutory deadline for the filing of the tax return and must be kept for at least five years from the end of the basis period in which the transaction took place. A person convicted of non-compliance under Section 34F will be subject to a fine not exceeding S$10,000. The o ence may be compounded by the Comptroller of Income Tax.

Taxpayers that are not required to prepare mandatory TP documentation under Section 34F of the ITA are nevertheless still required to ensure that their RPTs are carried out at arm’s length prices. To better manage transfer pricing risk, taxpayers which do not have to prepare TP documentation under Section 34F of the ITA are nonetheless encouraged to do so using the TP Documentation Rules and the IRAS e-tax guide.

CbC reporting

Singapore-headquartered multinational enterprises (“MNEs”) whose consolidated group revenue for the preceding financial year is at least S$1.125 billion are required to file a CbC report with the IRAS. In determining the consolidated group revenue, all of the revenue that is reflected in the consolidated financial statements should be used. In addition, from the financial year 2022 onwards, the consolidated group revenue should include extraordinary income and gains from investment activities.

The ultimate parent entity (“UPE”) of the Singapore MNE group is its Reporting Entity for the purpose of filing the CbC report. The UPE is required to file the CbC report for all entities in the group within 12 months from the end of the UPE’s financial year. For example, if the UPE’s financial year ends in December, the CbC report relating to the financial period from 1 January 2025 to 31 December 2025 should be submitted to the IRAS by 31 December 2026.

With effect from financial years beginning on or after 1 January 2022, Reporting Entities must notify the IRAS of their obligation to file a CbC report within 3 months from the end of their financial year end.

A company is not required to notify the IRAS if it is either a Singapore Constituent Entity of a Singapore MNE group and it is not the Reporting Entity, or if it is a Singapore Constituent Entity of a foreign MNE group.

RPT reporting

With effect from YA 2018, taxpayers must submit the Form for Reporting Related Party Transactions (“RPT Form”) together with their income tax returns if the value of the RPTs disclosed in the financial statements for the financial period exceeds S$15 million.

The value of RPTs as disclosed in the financial statements is the aggregate of:

a. All amounts of RPT as reported in the Income Statement but excluding compensation paid to key management personnel and dividends; and

b. Year-end balances of loans and non-trade amounts due from / to all related parties.

The IRAS has said that it will use the information disclosed in the RPT Form to perform transfer pricing risk assessment.

From YA 2020, the RPT Form has been available as part of the income tax return (i.e., Form C). If the Form C-S or Form C-S (Lite) is submitted, the Company is not required to submit the RPT Form as the RPT Form is to be submitted with Form C.

Companies should review their RPTs to ensure compliance with arm’s length prices and the various reporting requirements.

BEPS 2.0 – Pillar One Developments in the IRAS e Tax Guide on Transfer Pricing

IRAS issued the Transfer Pricing Guidelines (Eighth Edition) on 19 November 2025, which incorporate selected elements of BEPS 2.0 Pillar One into Singapore’s

transfer pricing framework.

Pillar One Amount B has been implemented via a Simplified and Streamlined Approach (“SSA”) for baseline marketing and distribution activities on a pilot basis from 1 January 2026 to 31 December 2028.

Pillar One Amount A (residual profit reallocation to market jurisdictions) has not been implemented and does not affect Singapore transfer pricing rules at this stage.

IRAS has clarified that Singapore continues to apply the arm’s length principle, with Amount B serving as a simplification mechanism rather than a reallocation of taxing rights.

Please reach out to us if the Company requires any assistance relating to TP/ CbC reporting matters.

5. Singapore Withholding Tax (“WHT”)

We would like to take this opportunity to remind the Company about Singapore WHT obligations as, based on our experience, this is an area often overlooked by companies.

The SITA requires certain payments made to non-residents (including persons not known to be tax residents in Singapore) to be subject to WHT. Such payments include:

- interest, commission, fees or any other payments in connection with any loan or indebtedness;

- royalty or other payments for the use of or the right to use any movable property;

- payment for the use of or the right to use scientific, technical, industrial or commercial knowledge or information or for the rendering of assistance or service in Singapore relating to the application or use of such knowledge or information;

- technical assistance, service and management fees for services rendered in Singapore;

- rent or other payments for the use of any movable property;

- directors’ remuneration (excluding payments as an executive director);

- proceeds from the sale of any real property by a non-resident property trader; and

- distribution of taxable income made by REIT to unitholder who is a non-resident (other than an

individual).

The tax withheld must be paid, together with the submission of the relevant WHT return, to the IRAS by the 15th of the second month following the date of payment to the non-resident.

Generally, the date of payment refers to the earliest of the following dates:-

- When payment is due based on contract or agreement, or the date of the invoice in the absence of any contract or agreement (without consideration for credit terms);

- When payment is reinvested, accumulated, capitalised, credited to an account or otherwise dealt with on behalf of the non-resident; or

- When the actual payment is made.

Failure to do so will result in the imposition of a penalty of up to 20% of the WHT outstanding.

If the Company has made or expects to make payments to non-residents and would like us to determine whether Singapore WHT applies, please reach out to us so that we can advise the Company accordingly.

6. Tax Clearance For Foreign Employees (Non-Singapore Citizens)

Generally, an employer is required to perform tax clearance for his foreign employee where his contract for work is about to end, or when he decides to work for another company or plans to leave Singapore for more than 3 months (unless the departure is on a regular basis in the course of his employment). The employer is statutorily required to complete and file the Form IR21 at least 1 month before the date of cessation of employment or departure from Singapore. Any late submission of the Form IR21 by the employer without valid reason(s) may result in the imposition of a fine not exceeding S$5,000 by the IRAS.

In addition, the employer is also required to withhold all monies that are due to the employee from the day that he notifies the employer of his intention to cease employment or when the employer notifies the employee of the termination of his employment or posting to an overseas location. The IRAS will process the Form IR21 and inform the employer to settle the income tax liability of the

employee.

Please reach out to us if the Company requires assistance on Singapore tax clearance for foreign employees.

7. Goods and Services Tax (”GST”) Registration

Compulsory GST registration

All businesses in Singapore are required to continually assess whether they are compulsorily required to register for GST. Compulsory registration is required when the taxable turnover (i.e., the annual value of the taxable supplies made) exceeds S$1 million. Businesses may be liable to register for GST under the retrospective view or prospective view.

Prior to 1 January 2019, compulsory registration under the retrospective view was required where the taxable turnover at the end of the calendar quarter (i.e., 3 months ending March, June, September or December) and the past three quarters exceeded S$1 million.

From 1 January 2019, compulsory registration is required under the retrospective view where the taxable turnover at the end of any calendar year (i.e., 31 December) exceeds S$1 million.

Under the prospective view, when at any point in time, there is certainty that the taxable turnover in the next 12 months will exceed S$1 million, compulsory registration is required.

The application for GST registration must be made within 30 days from the day the obligation to register for GST arises. Failure to do so may result in the imposition of fines and penalties by the IRAS.

GST registration relating to imported services and low-value goods

Under the reverse charge mechanism for Business-to-Business (“B2B”) imports, a local business may become liable for GST registration if its taxable turnover and/or the total value of its imported services and low-value goods exceeds S$ 1 million for a 12-month period, and the business would not be entitled to full input tax credit even if the business were GST-registered.

Under the OVR regime for Business-to-Consumer (“B2C”) supplies of remote services and low-value goods, an overseas supplier is liable for GST registration if its global annual turnover exceeds S$1 million and the value of its B2C supplies of remote services and/or low-value goods made to non-GST registered customers (including individuals and businesses that are not registered for GST) in Singapore exceeds S$100,000.

Where certain conditions are fulfilled, a local or overseas operator of an electronic marketplace may be regarded as the supplier of B2C supplies of remote services made by overseas suppliers and low-value goods made by local and overseas suppliers through its marketplace. In such cases, the local or overseas operator is required to include the value of such B2C services made to customers in Singapore to determine its GST registration liability.

Voluntary GST registration

A business that is not required to register for GST (including an overseas supplier or electronic marketplace operator that does not cross the registration threshold) may apply for voluntary registration subject to conditions. Once the business is voluntarily registered for GST, it must remain registered for at least 2 years.

Implementation of InvoiceNow for GST-Registered Businesses

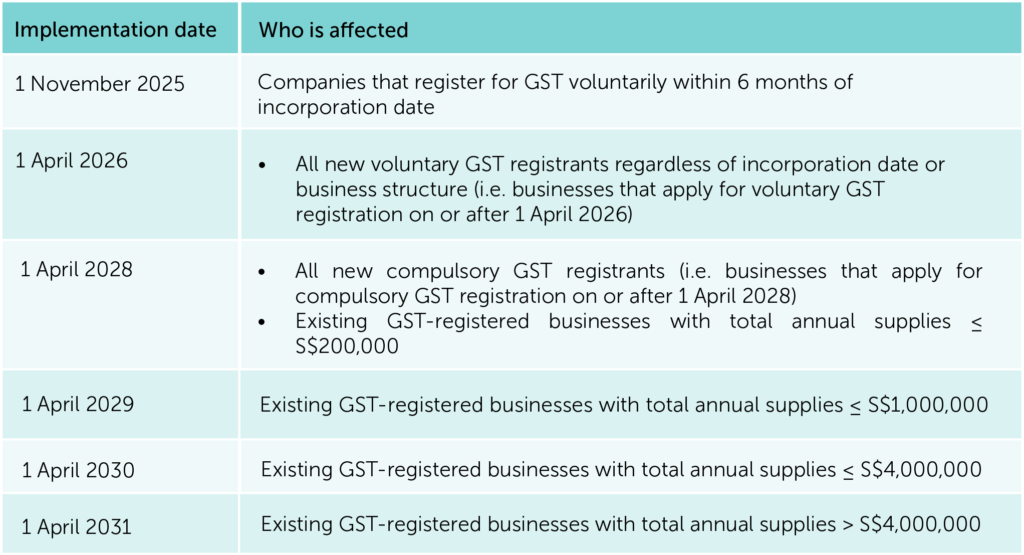

GST-registered businesses, unless exempted, will be required to transmit invoice data to the IRAS using InvoiceNow-Ready solutions via the InvoiceNow network. This requirement is introduced progressively as follows:

GST-registered businesses that were registered before 2026 will be informed by the IRAS of their respective implementation date by mid-2026.

Overseas entities and businesses liable to register for GST wholly due to the Reverse Charge regime are exempted from the InvoiceNow requirement.

The adoption of InvoiceNow is to support businesses in meeting their obligations as GST-registered entities by streamlining record-keeping, billing, and payment processes.

If the Company requires our assistance on GST registration, please contact us.

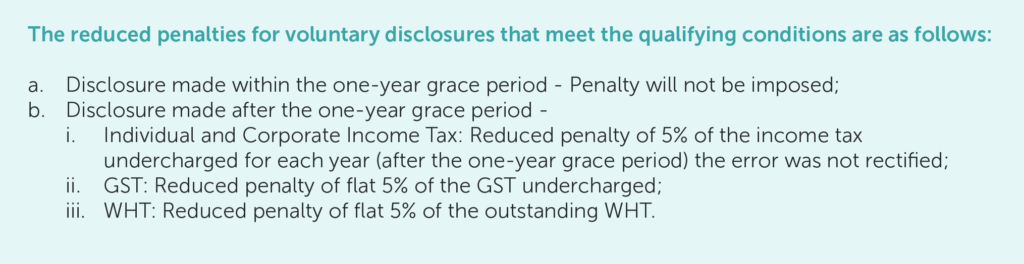

8. Voluntary Disclosure Programme (“VDP”)

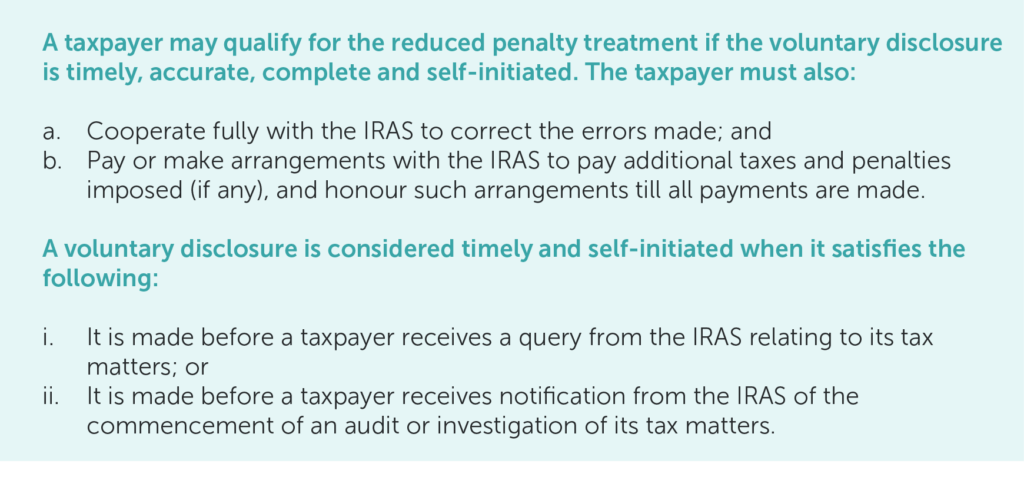

The VDP aims to encourage taxpayers that have made errors in their tax returns to voluntarily come forward to correct their errors and set their tax matters right, in exchange for reduced penalties.

The VDP is applicable to Income Tax, GST, WHT and Stamp Duty (“SD”).

For a taxpayer that has already received a query or is already under the IRAS’ audit or investigation, the disclosure must not fall within the immediate scope of the query, audit or investigation.

A VDP application will only be considered as complete when all information is submitted to the IRAS. For a list of information requested, please refer to the IRAS’ e-Tax Guide on the Voluntary Disclosure Programme.

Regardless of the frequency of voluntary disclosures made by a taxpayer, all voluntary disclosures meeting the qualifying conditions may be accorded reduced penalties depending on whether the disclosures are made within or after the 1-year grace period.

For a voluntary disclosure pertaining to late stamping or underpayment of SD that meets the qualifying conditions, the reduced penalty is 5% per annum computed on a daily basis on the SD payable. There is no grace period applicable to SD.

If the Company requires our assistance on matters pertaining to VDP, please feel free to contact us for a discussion.

As outlined in our letter of engagement for corporate tax compliance services, our scope of annual corporate tax compliance services covers the filing of ECI, and the preparation and submission of the income tax return and income tax computation to the IRAS. We

would be pleased, if the Company so instructs, to provide other tax services such as calculation of ECI, filing of withholding tax returns, MTT/DTT returns and GST returns, tax clearance for employees, tax advisory and transfer pricing services, etc.

View the full article in PDF here.

Contact Us

CLA Global TS Tax Advisory Specialists

|

Edwin Leow Head of Tax, Co- Advisory Leader edwinleow@sg.cla-ts.com |

|

Shaun Zheng Asset Management and Private Wealth Services Tax Lead shaunzheng@sg.cla-ts.com |

|

Koy Su Hiang Business & International Tax Lead koysuhiang@sg.cla-ts.com |

|

Jennifer Lee GST Tax Lead jenniferlee@sg.cla-ts.com |

|

John Chua Merger & Acquisitions Tax Lead johnchua@sg.cla-ts.com |

|

Belinda Lim Transfer Pricing Tax Lead belindalim@sg.cla-ts.com |

|

Jason Oon Governance and Sustainability Tax Lead jasonoon@sg.cla-ts.com |

|

Aaron Zhou Chinese Clients Tax Lead aaronzhou@sg.cla-ts.com |

|

Tan Xin Yi Individual Tax Lead tanxinyi@sg.cla-ts.com |

|

Else Guo Private Wealth Services Tax Specialist elseguo@sg.cla-ts.com |

|

Chris Lim Business Tax Specialist chrislim@sg.cla-ts.com |