Section 10L: A Substance-Based Shift in Singapore’s Capital Gains Landscape

For decades, Singapore has never imposed a standalone or comprehensive capital gains tax on individuals or companies. As at 1 January 2024, this long-standing position is no longer universally applicable for companies.

The introduction of Section 10L of the Income Tax Act (“ITA”) marks an evolution in Singapore’s tax framework. Instead of imposing a broad-based capital gains tax, Section 10L focuses on whether a Singapore entity has real economic substance, drawing a distinction between genuine commercial structures and arrangements that lack sufficient economic substance in Singapore.

As a result, the analysis is no longer just centred on whether a gain is “capital” or “revenue” in nature. Instead, greater emphasis is placed on substance over form; including where decisions are made, how activities are carried out, and whether value is genuinely created in Singapore. This marks a careful but meaningful refinement in how Singapore approaches the taxation of foreign‑sourced disposal gains and aligning itself to global standards in addressing international tax avoidance risks relating to foreign disposal gains parked in low-substance hubs.

Key Mechanism of Section 10L

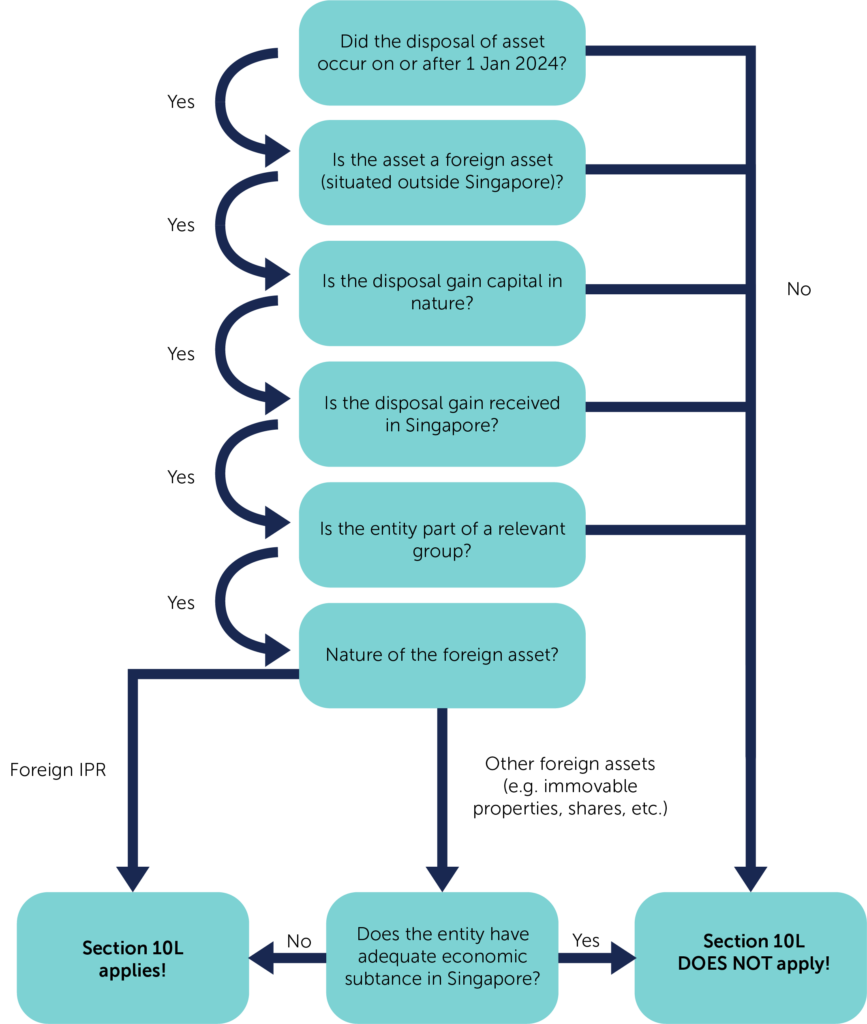

At its core, Section 10L treats foreign-sourced disposal gains as income chargeable to tax under Section 10(1)(g) of the ITA when they are received / deemed received in Singapore, regardless of whether they are capital in nature. Notably, this regime targets only covered entities i.e., entities that belong to a relevant group, broadly defined as groups with at least one entity operating or established outside Singapore. Purely domestic Singapore‑only groups are intentionally excluded from the regime.

Economic Substance as the central test

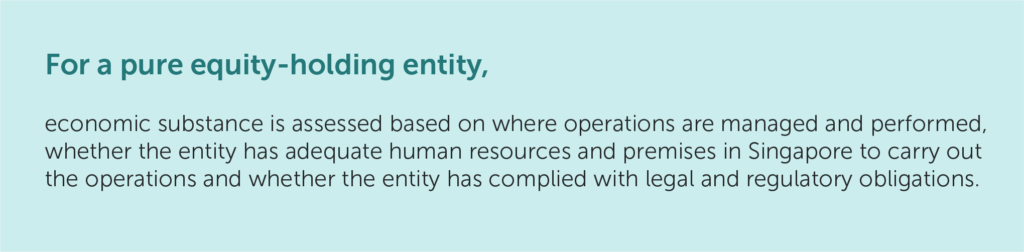

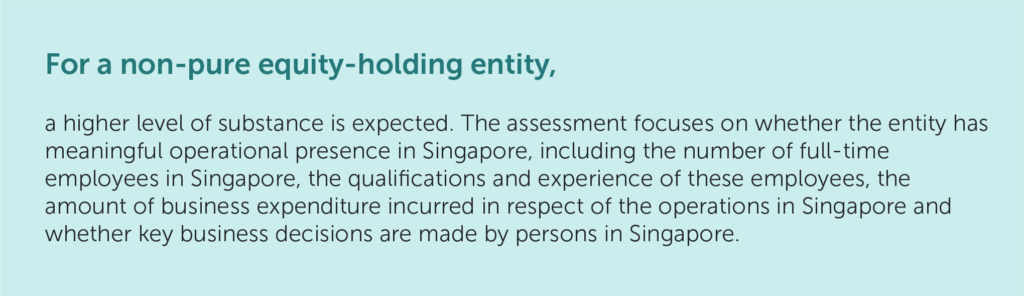

The cornerstone of Section 10L is the concept of economic substance. For disposals of foreign assets (other than Intellectual Property Rights), gains will not be taxed if the disposing entity can demonstrate adequate economic substance in Singapore during the basis period of the sale.

Stricter Treatment for Intellectual Property (“IP”)

Foreign IP tells a different story. Section 10L takes a much firmer stance here. Gains from the disposal of foreign IP rights are taxable regardless of economic substance. For groups with IP holding or licensing structures, this underscores the importance of careful planning, particularly where disposal proceeds are intended to be remitted to Singapore.

Closing thought

Section 10L does not mark the end of Singapore’s capital gains-friendly regime, but rather a refinement of it. In today’s environment, the key question is no longer whether a gain is capital in nature, but whether the entity earning that gain can demonstrate genuine economic presence in Singapore.

Entities with substantive governance, decision-making, and operational presence in Singapore may continue to fall outside its scope, while structures driven primarily by treating Singapore as a convenient tax-free exit hub are likely to face greater scrutiny.

Flowchart to assess applicability of Section 10L

How we can help

Navigating Section 10L requires more than identifying whether a disposal has occurred; it requires a holistic understanding of structure, substance, and transaction design. To support cross‑border groups, we offer a Section 10L Readiness Assessment tailored to identify risks early and provide defensible outcomes. This includes:

- Group structure review: Assessing whether the group falls within the scope of Section 10L.

- Economic substance assessment: Evaluation of the applicability and satisfaction of the economic substance requirements based on the company’s actual facts and circumstances.

- Advance ruling support: Where required, assisting with the preparation of advance ruling applications and proactive engagement with IRAS to obtain clarity on Section 10L position(s).

- Exit strategy considerations: Structural advice to assess and address the potential Singapore tax implications of foreign disposal gains under Section 10L.

View the full article in PDF here.

CONTACT US

CLA Global TS Tax Advisory Specialists

|

Edwin Leow Co-Advisory Leader Director, Head of Tax edwinleow@sg.cla-ts.com |

|

Shaun Zheng Director, Tax shaunzheng@sg.cla-ts.com |

|

Tan Xin Yi Manager, Tax tanxinyi@sg.cla-ts.com |