Driving Greater Accuracy in Group-Level Financial Reporting

As organisations expand across markets and establish new subsidiaries, joint ventures, and structured entities, the process of preparing consolidated financial statements becomes increasingly complex. Regulatory scrutiny continues to rise, and stakeholders demand higher transparency and faster reporting cycles. Inaccuracies in consolidation can lead to material misstatements, audit challenges, delayed filings, and reputational risk.

Hence, it is crucial for finance teams to avoid common pitfalls and strengthen the quality, reliability, and governance of the consolidation process.

The article is addressed to in-house finance team and not for outsourced accountants.

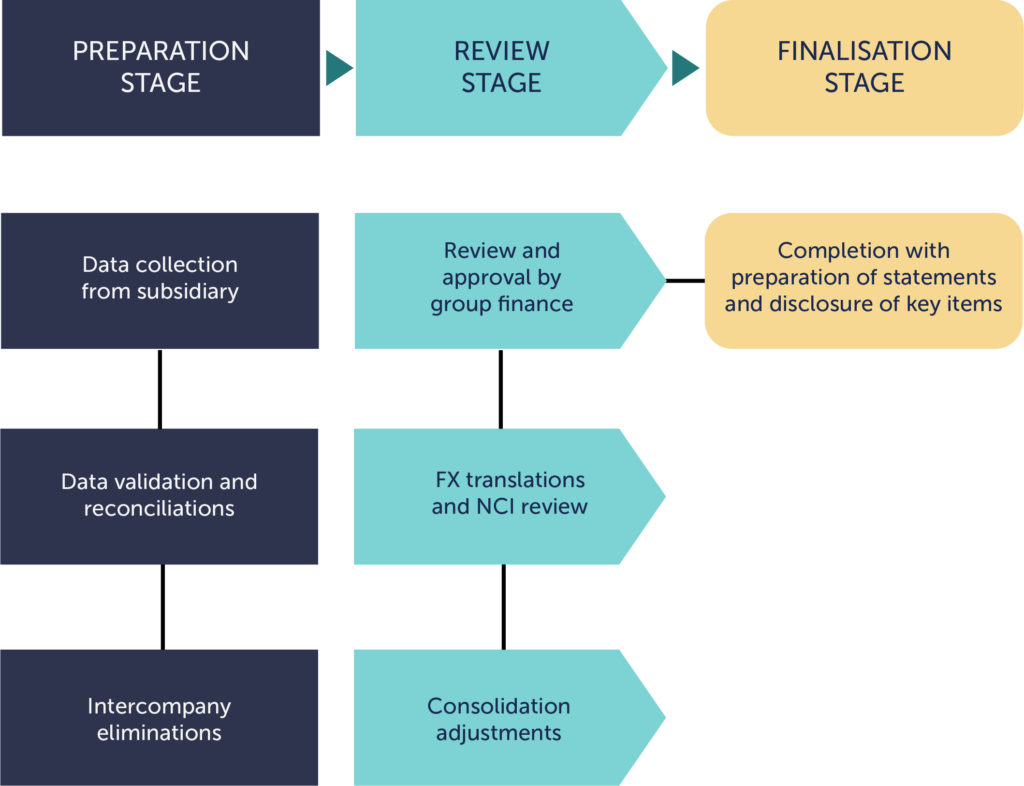

Consolidation Process Flow

The diagram below summarises the end-to-end consolidation journey—from subsidiary data capture to final financial statements.

Key Pitfalls

1. Incorrect Identification of Entities to Consolidate

Many consolidation issues begin with incorrectly identifying which entities should be included in the group. Errors occur when dormant subsidiaries or entities with indirect ownership are overlooked, or when investments are misclassified as associates despite the group exercising effective control. In some cases, the finance team may not reassess control even when voting rights, shareholder agreements, or contractual terms change.

Why it matters

Incorrect entity identification leads to incomplete financials and potential non-compliance with accounting standards.

2. Inconsistent Accounting Policies Across Entities

A frequent challenge arises when subsidiaries follow differing accounting policies, especially where local GAAP applies. Variations in revenue recognition, depreciation methods, and impairment assessments create inconsistencies that distort consolidated figures. Inadequate documentation or inconsistent application of alignment adjustments further compounds the issue.

Why it matters

Lack of policy alignment undermines comparability and complicates the audit process.

3. Errors in Intercompany Elimination

Intercompany mismatches remain one of the most persistent pain points in consolidation. Timing differences, currency translation issues, or incorrect account mapping often cause discrepancies in receivables, payables, revenue, and cost eliminations. Unrealised profits from intra-group inventory transfers or asset sales are sometimes overlooked, as are intercompany interest and loan reconciliations.

Why it matters

Unresolved mismatches distort group results and create avoidable audit findings.

4. Foreign Currency Translation Issues

Errors commonly occur when teams use incorrect exchange rates or apply average and closing rates inconsistently. Miscalculations in translation reserves, particularly when entities are disposed of or restructured, can have significant impacts on equity. Some teams also overlook the need for hyperinflation accounting in certain jurisdictions.

Why it matters

FX errors can materially affect both the income statement and other comprehensive income.

5. Incomplete or Incorrect Purchase Price Allocation (PPA)

Acquisition accounting often breaks down when teams do not fully identify intangible assets, overstate goodwill, or omit contingent consideration such as earn-outs. Weak governance during the measurement period may result in missed fair value adjustments.

Why it matters

Incorrect PPAs affect future earnings, amortisation, impairment testing, and overall financial transparency.

6. Weak Controls Over Manual Top-Side Journals

Reliance on manual adjustments increases the risk of unclear ownership, insufficient documentation, and errors. Some adjustments are posted directly into consolidated results without validation from entity teams or without clear explanations.

Why it matters

Lack of control over manual journals is a leading cause of audit adjustments and control deficiencies.

7. Insufficient Review of Non-Controlling Interests (NCI)

NCI calculations become complex when ownership changes mid-year or when put/call options and variable interests are involved. Inaccuracies in the allocation of profit, OCI, and equity can significantly distort reported group ownership.

Why it matters

Incorrect NCI reporting misrepresents true ownership and profit attribution.

8. Delays or Poor-Quality Reporting from Subsidiaries

Late submissions, incomplete disclosure templates, and inconsistent formats can delay consolidation timelines and force rushed reviews. Newly acquired or smaller subsidiaries are often the biggest contributors to reporting inconsistencies.

Why it matters

The quality and timeliness of subsidiary data determine the quality and speed of group financial reporting.

9. Inadequate Disclosure Preparation

Disclosure preparation is frequently left to the end of the reporting cycle, resulting in incomplete related-party disclosures, insufficient explanations of judgements and estimates, and outdated notes on group structure.

Why it matters

Weak disclosures signal poor governance and increase regulatory and audit risk.

10. Weak Governance Over Consolidation Systems

Errors frequently arise from outdated chart-of-accounts mappings, insufficient integration between ERP systems and the consolidation tool, or lax user access controls. When system logic is not periodically reviewed, incorrect classifications can go undetected for extended periods.

Why it matters

Strong system governance ensures consistency, accuracy, and control throughout the reporting process.

Strengthening the Consolidation Process

1. Process & Governance

- Establish formal consolidation calendar with clear deadlines and escalation protocols.

- Assign ownership for key stages.

- Conduct periodic dry‑run consolidations ahead of year‑end.

2. Systems & Automation

- Implement automated intercompany reconciliation and elimination tools.

- Review chart‑of‑accounts mappings annually.

- Strengthen system access controls with regular reviews.

3. Subsidiary Engagement

- Standardise reporting templates across all entities.

- Provide ongoing training for smaller or newly acquired finance teams.

- Require pre‑submission certifications from each subsidiary CFO or Controller.

4. Quality & Assurance

- Increase review frequency for NCI, PPA, FX translation, and complex adjustments.

- Maintain comprehensive documentation for all manual top‑side journals.

- Engage auditors early on complex transactions.

Summary

High-quality consolidated financial statements depend not only on accounting expertise but also on strong governance, disciplined processes, and reliable data inputs. By addressing the pitfalls outlined in this advisory and embedding structured, repeatable practices, finance teams can enhance reporting accuracy, reduce audit findings, and build greater confidence among stakeholders.

We are here to help. If you have been dealing with persistent issues that keep resurfacing or taking up valuable time, talk to us. Our Outsourcing specialists can offer practical insights and recommend solutions to help you address the root causes and reduce ongoing pressure.

Contact our team of Outsourcing specialists for more details and specific guidance.

View the full article in PDF here.

CONTACT US

CLA Global TS Outsourcing Specialists

|

Grace Lui Co- Advisory Leader Director, Valuation, Transaction Services & Outsourcing gracelui@sg.cla-ts.com |

|

Esther Tan Associate Director, Outsourcing Services etan@sg.cla-ts.com |