In today’s dynamic economic landscape, companies are increasingly seeking opportunities to leverage strategic advantages for regional expansion and market improvement. The Johor-Singapore Special Economic Zone (JS-SEZ) presents a unique opportunity for businesses to capitalize on Singapore’s esteemed position in global and regional markets, fostering growth and expansion. To maximize the potential of venturing into this neighbouring market, companies must carefully consider essential aspects of business expansion, including legal requirements, compliance, financial reporting, and tax implications.

Business Incorporation in Malaysia

To be recognised as a legitimate entity in Malaysia, businesses must register with Suruhanjaya Syarikat Malaysia (SSM). This registration is essential for fundamental operational requirements, such as opening bank accounts, registering for tax, and applying for business licenses. It also builds credibility and trust among Malaysian customers, suppliers, and partners.

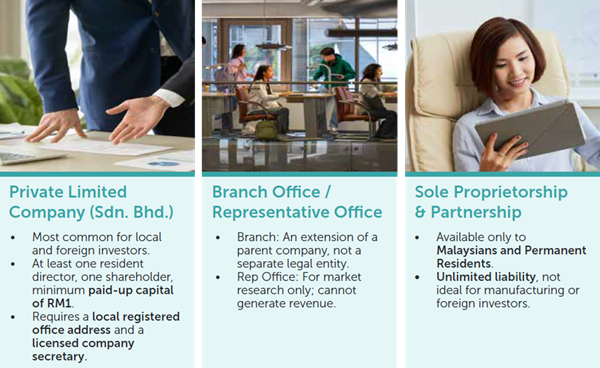

Types of Business Entities in Malaysia

Choosing the appropriate business structure is vital for a successful market entry. The common types include:

Among these, the Sdn. Bhd. is the most common and recommended structure for foreign and manufacturing businesses. It offers limited liability, operates as a separate legal entity from its parent company, and allows full foreign ownership in most sectors—facilitating capital raising and business scalability.

Post-Incorporation Obligations

To have a fully functional and operational entity, companies should also take note of the Post-Incorporation Requirements, specifically the following points:

- Tax Registration with LHDN (Inland Revenue).

- Employee-related Registrations: EPF, SOCSO, HRDF.

- Local Authority Licenses: Business premise and signage.

- Industry-Specific Licenses: Required depending on business activities (e.g. F&B, healthcare, education, etc)

Compliance and Financial Reporting Considerations

In order to expand abroad, companies need to be informed of the important compliance and financial reporting considerations between both countries to ensure smooth operationality of the business.

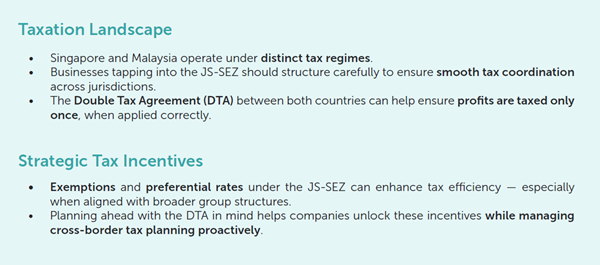

Cross-Border Taxation and Double Taxation Agreements (DTA)

Transfer Pricing

Businesses that operate across Singapore and Malaysia often engage in transactions with related parties.

These arrangements may require companies to apply transfer pricing principles to ensure that intercompany pricing is commercially justifiable and in line with arm’s length standards set by Malaysian regulations.

Early planning and documentation provide strong support in the event of a tax review or audit.

Currency Exchange and Hedging

Financial Reporting and Consolidation

While expanding to Malaysia or vice versa, companies are to note the differences in accounting standards. Singapore follows the Singapore Financial Reporting Standards (SFRS), while Malaysia uses the Malaysian Financial Reporting Standards (MFRS), both of which are largely aligned to International Financial Reporting Standards (IFRS).

For private, small and medium-sized entities, companies may opt to apply the Singapore Financial Reporting Standards for Small Entities (SFRS for SE) in Singapore or the Malaysian Private Entity Reporting Standards (MPERS), if the criteria are met.

Business may need to consider how to consolidate financial statements or comply with both accounting standards, depending on their structure.

Other Potential Considerations

JS-SEZ Tax Considerations: Move Early, Move Strategically

As the Johor-Singapore Special Economic Zone (JS-SEZ) opens its doors, businesses eyeing expansion into Malaysia should view tax planning not as an afterthought — but as a strategic first

step.

Understanding the tax landscape in depth is key to unlocking long-term gains. Early planning enables companies to maximise incentives, avoid costly missteps, and build structures that scale with growth.

Maximising Tax Incentives: What’s on the Table

The Malaysian government has introduced aggressive, targeted incentives to draw high-value investments into the JS-SEZ:

- 5% corporate tax for up to 15 years

- 15% personal tax for foreign professionals

- Fast-track customs clearance and investment facilitation

But — and this is critical — these incentives are not automatic. They are subject to application, with approval hinging on your structure, timing, and declared activity.

Companies are well-advised to approach this as they would a grant application, not a routine company setup. Acting early — without assuming automatic eligibility — is essential to avoid missing a valuable window of opportunity.

Common Pitfalls: What to avoid

The most common errors stem from one mindset: “We will sort out tax later.” This approach risks the very benefits that make the JS-SEZ attractive.

Examples include:

The good news? These pitfalls are entirely avoidable — when tax is built into the plan from day one.

What this could look like in practice

A company begins operations in Johor — assuming their activity qualifies for the 5% tax rate.

Months later, they learn that their setup does not meet the Malaysian Investment Development Authority (MIDA) incentive conditions. By then, they have already missed the chance to apply at the right point in their project timeline.

The result? They default to the 24% corporate tax rate — and may struggle to restructure without triggering penalties or compliance issues.

These are the avoidable mistakes we help clients plan around.

Structure that scales with growth

Whether your company already has a presence in Malaysia or is entering for the first time, eligibility is assessed on a per-project basis.

This means:

- A new manufacturing line,

- A regional HQ function, or

- An expansion into high-value services.

…may all qualify independently — even if your core business is already operational in Malaysia.

What matters is how the activity is framed, timed, and structured.

The Bottom Line

The JS-SEZ is not just about tax savings — it is about positioning your business for sustainable regional growth.

To fully unlock the value, early advisory makes the difference — not just in qualifying for incentives, but in designing a structure that works now and scales later.

If your company is planning, reviewing, or even just exploring operations in Johor — now is the time to start the conversation. We can help assess eligibility, align timing, and ensure tax supports your long-term strategy — not slows it down.

How CLA Global TS Can Help You

The Johor-Singapore Special Economic Zone (JS-SEZ) offers significant potential — not just in tax incentives, but in creating a strategic base for regional operations.

While the benefits are attractive, realizing them requires more than a company setup. Businesses must navigate due diligence, eligibility criteria, structuring, and timelines to succeed.

That is where CLA Global TS can help.

Our multi-disciplinary team is equipped to support you across tax, regulatory, and operational aspects of cross-border expansion. Whether you are entering Malaysia for the first time or scaling up existing operations, we will work with you to support a structure that is compliant, efficient, and future-ready — ensuring your move is seamless, informed, and aligned with long-term goals.

View the full article in PDF here.

CONTACT US

CLA Global TS Business Advisors

Tax Advisory Specialists

|

Edwin Leow Co-Advisory Leader Director, Head of Tax edwinleow@sg.cla-ts.com |

|

Jason Oon Associate Director, Tax jasonoon@sg.cla-ts.com |

Financial Reporting Specialist

|

Sandy Hock Director, Assurance sandyhock@sg.cla-ts.com |

Corporate Secretariat Specialist

|

Loh Mei Ling Director, Corporate Services Corporate Secretarial & Bookkeeping Pte Ltd lohmeiling@csb.com.sg |