Executive Summary

- Recent tariff actions and customs scrutiny on Asian-origin goods mean related-party import pricing is under the spotlight.

- Transfer pricing documentation (TPD), while designed for tax, is increasingly reviewed by customs authorities to test declared import values.

- The WCO–OECD case studies show both outcomes: in one case, TPD helped secure acceptance; in another, margins outside industry norms led to rejection.

- For Singapore exporters, robust TPD can strengthen defensibility abroad, but it must be methodologically sound and commercially aligned.

- Businesses should review their TPD now — not only to satisfy IRAS, but also to manage cross-border customs risk.

Rising Scrutiny on Related-Party Imports

With tariff actions and heightened customs controls on goods of Asian origin, multinational groups face growing pressure on how they set and defend their

related-party prices. For Singapore exporters selling to affliates abroad, transfer pricing (TP) documentation prepared for IRAS compliance is increasingly being reviewed in customs contexts—particularly where authorities ask: was the declared import value influenced by the relationship?

Why TP Documentation Matters Beyond Tax

Although TP and customs rules serve different objectives, both examine related-party prices. Tax authorities focus on whether profits are shifted out of their jurisdiction, while customs authorities worry about undervaluation that erodes duty revenue. This tension creates risk, but also opportunity: robust TP documentation can sometimes help demonstrate that declared import prices are consistent with market outcomes.

The WCO–OECD Guide to Customs Valuation and Transfer Pricing illustrates this through practical case studies.

Two examples—Case 14.1 and Case 14.2—show both the potential and the limitations of relying on TP documentation for customs purposes.

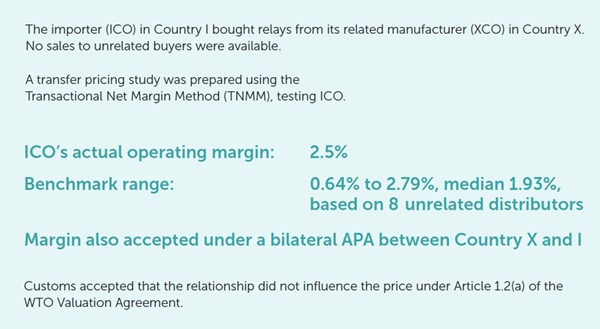

Case Study 14.1

When TP Documentation Supported the Declared Value

Takeaway

When no third-party sales are available, a TNMM-based TP study—particularly one aligned with an APA—can support that the declared import value reflects arm’s length conditions.

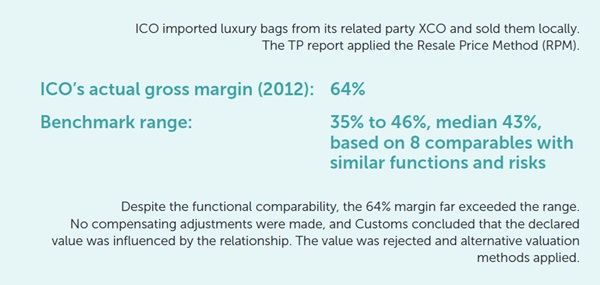

Case Study 14.2

When TP Documentation Fell Short

Takeaway

Even with suitable comparables, TP documentation may not protect the declared value if actual outcomes diverge too far from market benchmarks.

Relevance for Singapore Exporters

For Singapore-based exporters, TP documentation is not automatically accepted for customs purposes, but it can serve as valuable support where:

- Third-party sales are unavailable, and

- Authorities want evidence that related-party pricing aligns with industry norms.

This is particularly relevant for electronics, branded consumer goods, and apparel, where origin-sensitive audits are intensifying in markets such as the U.S.

Our Perspective

At CLA Global TS, we help clients prepare clear, defensible TP documentation that satisfies Singapore requirements and also strengthens the company’s position in cross-border customs discussions. While we do not represent clients before customs authorities, we coordinate with in-market advisors to build a consistent and defensible narrative.

Speak with our Tax Specialists today and begin your TP documentation and strengthen your company’s cross-border customs position.

View the full article in PDF here.

CONTACT US

CLA Global TS Business Advisors

Tax Advisory Specialists

|

Edwin Leow Co-Advisory Leader Director, Head of Tax edwinleow@sg.cla-ts.com |

|

Jason Oon Associate Director, Tax jasonoon@sg.cla-ts.com |