Effective 15 June 2026, the Monetary Authority of Singapore (“MAS”) has officially implemented its long-awaited revamped licensing exemption framework for Single Family Offices (“SFOs”). This new framework introduces a single, harmonised, and structure-agnostic class exemption, completely replacing the legacy “related corporations” exemption and previous case-by-case application pathways.

Core Qualifying Criteria

To rely on the new class exemption under the Securities and Futures (Licensing and Conduct of Business) Regulations, an SFO must satisfy the following mandatory structural and operational conditions:

- Singapore Incorporation

The SFO must be a private company limited by shares incorporated in Singapore. - Exclusive Family Funding & Ownership

The SFO must be wholly owned (directly or indirectly) and funded exclusively by members of a single family. It is highly flexible and structure-agnostic, meaning it can sit underneath a trust, holding company, or foundation, provided the capital ultimately originates from the family. - Scope of Fund Management

The SFO can only manage funds for or on behalf of family members, family trusts, corporations wholly owned by and for the sole benefit of the family, and charitable organisations funded exclusively by the family. - Key Employee Carve-outs

The SFO is permitted to manage assets originating from “Key Employees” (such as the CEO, Executive Directors, CFO, and investment professionals). However, these assets must not exceed 10% of the SFO’s total assets under management (“AUM”) in aggregate, and key employees are restricted to a non-controlling ownership stake of up to 10% in the SFO structure.

Key Clarifications From The MAS

The MAS has provided crucial guidance regarding the operational scope and technical definitions of the new framework:

The Five-Generation Rule

A “family member” is legally defined as all lineal descendants of a common ancestor (including current or former spouses, adopted children, and stepchildren). The common ancestor must be within five generations of the youngest generation at the point the SFO is established in Singapore. Once this condition is met at inception, all subsequent future generations (Generation 6 onwards) are permitted to be served by the SFO without restriction.

Anti-Money Laundering and Countering of Financing of Terrorism (“AML/CFT”) Anchors

To ensure robust oversight, both the SFO and its local fund vehicles are strictly required to open and maintain bank accounts with a MAS-licensed bank in Singapore. For foreign-incorporated fund vehicles, accounts can be maintained either with a MAS-licensed bank in Singapore or with a regulated bank in a foreign jurisdiction that complies with Financial Action Task Force (“FATF”) standards. Banks will apply a risk-based approach to conduct comprehensive customer due diligence and ongoing monitoring on these accounts. This effectively anchors regulatory oversight within MAS’ supervisory perimeter, even where fund vehicles are offshore.

Case-by-Case Licensing Exemptions Phased Out

MAS has explicitly stated that it will generally no longer grant case-by-case licensing exemptions unless exceptional circumstances exist. The framework’s structure-agnostic design is explicitly intended to accommodate varied family arrangements without requiring custom regulatory workarounds.

Compliance Obligations and Transition Timeline

For New SFOs

Annual Reporting Requirements

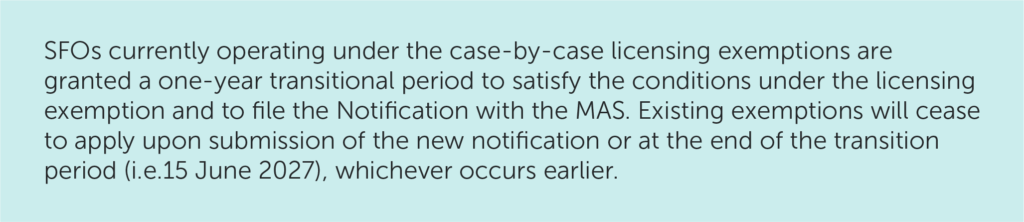

For Existing SFOs

Our Comments

“MAS’ adoption of a harmonised SFO exemption framework marks a significant shift towards rules‑based regulation, enhanced transparency, and greater supervisory consistency. By eliminating case‑by‑case licensing exemptions, the new framework provides clearer operating parameters while preserving Singapore’s competitiveness as a leading family office hub.

For existing SFOs, the transition period to 15 June 2027 is a critical window to validate structural eligibility and operational readiness. Immediate priorities include confirming compliance with the five‑generation family definition, verifying that all relevant entities maintain banking relationships with MAS‑licensed or FATF‑compliant institutions, and ensuring key employee participation (where implemented) remains within prescribed thresholds.

Early and proactive alignment will be essential to mitigate regulatory risk and ensure continuity of exemption status under the new framework.”

How CLA Global TS Can Assist

At CLA Global TS, we bring extensive and well-rounded experience in advising family office owners on navigating the New Harmonised Single Family Office Framework. We provide guidance on meeting the qualifying criteria and identifying key transition priorities to help you fully benefit from the framework.

Reach out to our Tax Specialists for in-depth insights on how to navigate these changes effectively and start your transition with confidence.

View the full article in PDF here.

CONTACT US

CLA Global TS Tax Specialists

|

Edwin Leow Co- Advisory Leader Director, Head of Tax edwinleow@sg.cla-ts.com |

|

Shaun Zheng Director, Tax shaunzheng@sg.cla-ts.com |

|

Aaron Zhou Associate Director, Tax aaronzhou@sg.cla-ts.com |

|

Tan Xin Yi Manager, Tax tanxinyi@sg.cla-ts.com |

|

Else Guo Manager, Tax elseguo@sg.cla-ts.com |

|

Penny Foo Assistant Manager, Tax pennyfoo@sg.cla-ts.com |