According to the Climate Review Report 2024 published by Singapore Exchange (SGX), 97% of listed issuers have adopted climate reporting aligned with the Taskforce for Climate-related Financial Disclosures (TCFD) framework. SGX had announced in September 2024 that for financial years beginning on or after 1 January 2025, listed companies are expected to transition to the International Financial Reporting Standards (IFRS) International Sustainability Standards Board (ISSB) standards, which have now taken over the TCFD’s work.

As of 25 August 2025, new requirements by the Accounting and Corporate Regulatory Authority (ACRA) and Singapore Exchange Regulation (SGX RegCo) have been introduced in SGX’s announcement.

As SGX still requires climate reporting and Scope 1 and 2 disclosure under the ISSB requirements for all issuers, what may your company need to do in preparation for the upcoming changes?

Impact of the Sustainability Reporting Changes

The key impact of these changes is that, for climate-related reporting — one of the six primary components of the sustainability report — there will be changes in the implementation of the new ISSB standards, Scope 3 reporting, and limited assurance requirements.

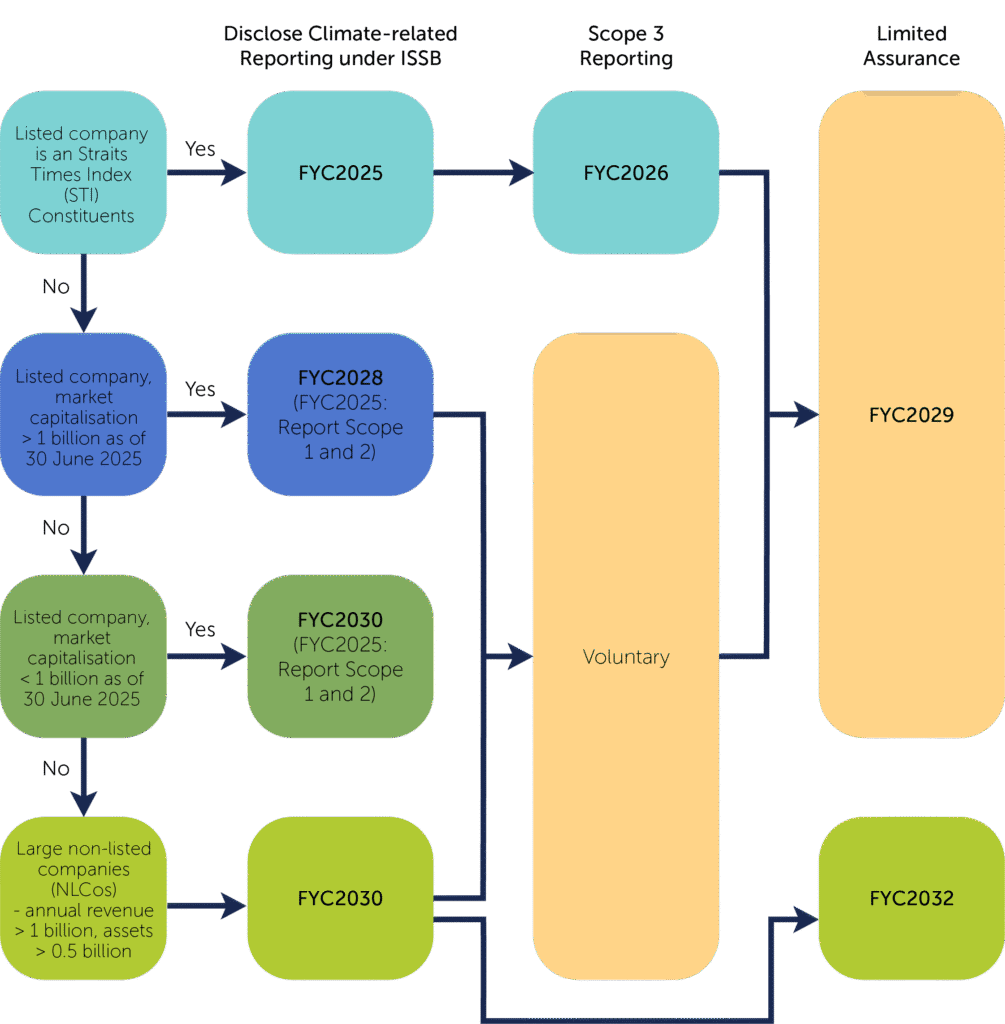

The flowchart below summarises the requirements and outlines the scope of changes for quick reference.

FYC202X denotes the year commencing on or after 1 January 202X.

Key Impacts on Companies

The changes in reporting requirements allow more runway for companies to plan and strategise on how best to include the ISSB requirements on climate reporting.

Companies will also be able to engage their auditors to discuss the requirements of audits and where possible, to commence with a subset of the Scope 1 and 2 assurance – this allows them to take advantage of the Sustainability Reporting (SR) grant by Enterprise Development Grant (EDG) and Enterprise Singapore.

Instead of focusing on reporting, companies are able to review internal processes to incorporate green elements such as green finance, transition planning.

Customers may be increasingly requesting companies to comply with standards such as Carbon Disclosure Project (CDP), Science Based Targets initiative (SBTi) and more efforts can be put into improving performance in these areas.

It is important to note that:

- Under SGX Rule 711A, a sustainability report is still required to be published.

- Climate-related reporting (for most listed companies, this means Scope 1 and 2 emission reporting) is still a requirement under the Rule 711(b) and must adhere to the Practice Note 7.6/7F.

How Can CLA Global TS Help

Before the full ISSB requirements kick in, CLA Global TS can help in performing gap analysis or optimising current Sustainability Reporting. Our Sustainability and Climate Change Specialists can assist in integrating climate requirements into your strategy, roadmap and risk management systems.

We can also help in developing a roadmap to meet ISSB requirements so that disclosures can be phased in over the next few years.

For any questions or concerns regarding Sustainability and Climate Change matters, please reach out to our specialists.

View the full article in PDF here.

CONTACT US

Business Advisors

|

Pamela Chen Director, Head of Internal Audit, Sustainability & Climate Change pamelachen@sg.cla-ts.com |

|

Maria Teo Associate Director, Sustainability & Climate Change Lead, Risk Advisory mariateo@sg.cla-ts.com |