To date, during the third quarter of this year, various Chinese government bureaus have issued announcements regarding upgrades to existing Value-Added Tax (VAT) regulations and the withholding tax on foreign investor reinvestment in China. Additionally, the Shanghai Municipal Government has introduced a new policy aimed at incentivising basic research and technological advancement through subsidies for qualifying enterprises.

Improving the Policy for VAT Refund of Unused End-of-Period Input Tax Credits

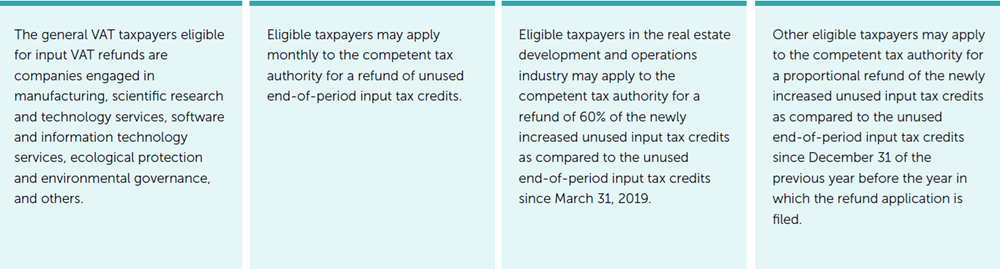

In late August, the Ministry of Finance (MOF) and the State Administration of Taxation (SAT) issued an announcement, Improving the Policy for VAT Refund of Unused End-of-Period Input Tax Credits, in which a new VAT refund policy for unused input tax credits in certain industries is discussed. The SAT then issued the Announcement of the State Taxation Administration on Matters Concerning the Administration of VAT Refund of Unused End-of-Period Input Tax Credits to clarify the administrative matters related to the refund of unused input tax credits. The new policy is effective as of September 1 of this year.

Highlights of the announcements include

Draft Implementation Regulations of the Value-Added Tax Law of the People’s Republic of China

Earlier in August, the MOF and SAT jointly issued an announcement to publicly solicit opinions on the Draft Implementation Regulations of the Value-Added Tax Law of the People’s Republic of China. This new draft consists of 57 articles in six chapters that include discussions of general provisions, tax rates, taxable amount, tax incentives, tax collection and administration, and supplementary provisions.

In the general provisions chapter, the draft further refines and clarifies the basic tax elements stipulated in the Value-Added Tax Law, such as the definitions of taxpayers and the taxable scope.

Regarding tax rates, the draft specifies the VAT considerations related to exported goods, cross-border sales of services, and intangible assets as prescribed by the VAT law.

The draft additionally elaborates on the applicable rules where multiple tax rates and collection rates are involved. As to tax incentives, the draft defines specific standards for VAT-exempt items specified in the Value-Added Tax Law. And with regards to collection and administration, the draft provides detailed regulations on the relevant provisions of the Value-Added Tax Law. The commenting period closes at the end of September.

Announcement on Matters Concerning the Tax Credit Policy for Foreign Investors Direct Investment with Distributed Profits

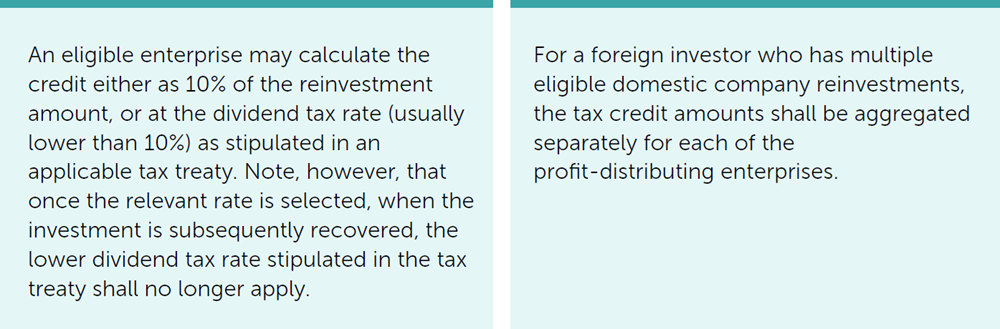

Also in August, the SAT issued the Announcement on Matters Concerning the Tax Credit Policy for Foreign Investors Direct Investment with Distributed Profits. The new policies shall come into force as of January 1, 2025. Where regulations generally treat reinvestments as distributed profits liable to dividend withholding tax, eligible reinvestments are now eligible for withholding tax refunds.

That is, when foreign investors make reinvestments using distributed profits that have been subject to withholding tax, a tax credit amount shall be calculated as distinguished in the following two scenarios:

Strengthening Basic Research and Enhancing New Momentum for High-Quality Development

Lastly, the General Office of the Shanghai Municipal People’s Government recently issued a favorable incentive policy titled Several Measures of Shanghai Municipality to Support Enterprises in Strengthening Basic Research and Enhancing New Momentum for High-Quality Development. The policy came into effect on August 1, 2025 and will remain in effect for five years until July 31, 2030.

The measures include tax incentives to support enterprise investment in basic research. For enterprises that provide funding for basic research by non-profit research institutions, universities, and government-funded natural science foundations, the actual amount incurred may be deducted before tax when calculating taxable income. An additional 100% pre-tax deduction is also allowed. Non-profit research institutions and universities that receive funds for basic research from enterprises, individuals, and other organizations shall be exempt from corporate income tax.

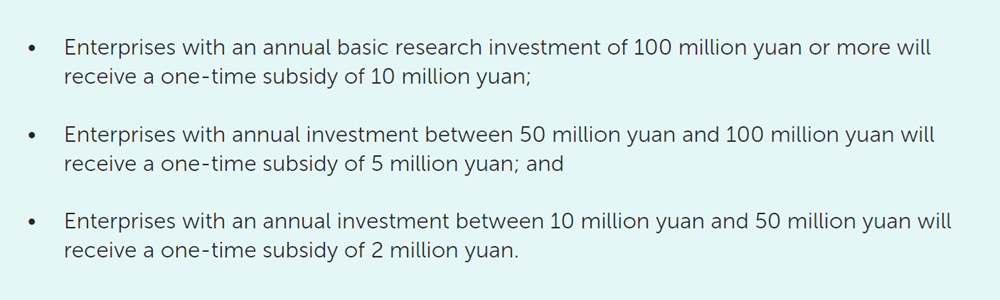

Further, to encourage enterprise investment in basic research and strengthen technology reserves, one-time financial subsidies will be granted as follows to eligible enterprises:

As is evident these and other policies released in the last year, China is continuing to update and upgrade its tax systems, as well as to promote both foreign direct investment (FDI) and investment in new and high technology. In addition to the anticipated release of the new VAT implementation regulations discussed above, it is expected that further upgrades to FDI and technology-related incentives shall also be released before year’s end.

If you have any questions or concerns regarding the latest tax and business developments in China, please contact our business advisors at CLA Global TS (Shanghai) Co., Ltd.

View the full article in PDF here.

CONTACT US

CLA Global TS Business Advisors

|

Flora Luo Director, Foreign Investment, China Tax and Legal Advisory CLA Global TS (Shanghai) Co., Ltd floraluo@cn.cla-ts.com |

|

Dr Scott Heidecke Senior Consultant CLA Global TS (Shanghai) Co., Ltd scott@cn.cla-ts.com |