Understanding How ESG drives Future Growth and Value

As the region emerges from the recent wave of COVID-19, with supporting policies of pandemic lifted, the risks associated with supply-chain disruptions, high borrowing rates, geopolitical tensions, financial market risks and changing regulations, may play out across the diverse economies of Asia. Hence, investors are increasingly applying non-financial factors such as Environmental, Social, and Governance (ESG) as part of their analysis process to identify material risks and growth opportunities. Numerous institutions, such as the Sustainability Accounting Standards Board (SASB), the Global Reporting Initiative (GRI), and the Task Force on Climate-related Financial Disclosures (TCFD) are working to form standards and define materiality to facilitate incorporation of these factors into the investment process.

Global Reporting Initiative (“GRI”) Standards in Sustainability Reporting

ESG metrics are not commonly part of mandatory financial reporting, though companies are increasingly making disclosures in their annual report or in a standalone sustainability report. The Singapore Exchange has been advocating for listed companies to prepare sustainability reports to improve on public disclosure obligations in accordance with the Global Reporting Initiative (“GRI”) Standards Sustainability Reporting Guidelines 2016 – Core Option and its reporting principles. GRI standards continue to be the sustainability reporting framework of choice as it is a globally recognised standard, to provide a broad and comparable disclosure of the ESG performance. GRI 2021 will be effective for information published on or after 1 January 2023, particularly to IFRS S1 and IFRS S2. Public listed companies are required to prepare an annual sustainability report which must include the primary components as set out in Listing Rule 711B on a ‘comply or explain’ basis (other than as required under Listing Rule 711B(2)).

IFRS S1: General Sustainability Disclosures

To provide information about significant sustainability-related risks and opportunities to assist primary users of general-purpose financial reporting when they assess enterprise value and decide whether to provide resources to the company.

IFRS S2: Climate-Related Disclosures

To provide information about exposure to climate-related risks and opportunities to assist users in assessing effects on enterprise value, understanding use of resources, and evaluating strategy, business model, and operational adaptation abilities.

ESG governance standards ensure a company uses accurate and transparent accounting methods, pursues integrity and diversity in selecting its leadership, and is accountable to shareholders.

What constitutes ESG Factors?

Conservation of the natural world that includes Climate change and carbon emissions, Air and water pollution, Energy efficiency and Water scarcity, consideration of people and relationships that includes customer satisfaction, Data protection and privacy, and Gender and diversity, and standards for running a company that encompasses Board composition, Audit committee structure, political contributions and Whistleblower schemes.

Benefits of having a strong ESG Proposition

Global warming is real. Visible signs of climate change, spread of infectious diseases such as Covid-19 and monkeypox have revealed the importance of ESG factors in today’s valuation.

A strong ESG proposition will enable companies to tap into new markets and expand into existing ones with governing authorities more likely to approve and licensed based on the prior performance in sustainability. Further, company can enhance the investment returns by having more sustainable plant and equipment for the long term as well as avoid investments that may not pay off because of longer-term environmental issues. Company can also achieve better access to resources through stronger community and government relations that will boost employee motivation and attract talent through greater social credibility. Having ESG in mind and being proactive about environmental risk can be a source of competitive advantage companies when they seek to reformulate products to prevent pollution, improve manufacturing processes, redesign equipment, and recycle and reuse waste from production.

A strong ESG proposition can help companies attract and retain quality employees, enhance employee motivation by instilling a sense of purpose, and increase productivity overall. Employee satisfaction is positively correlated with shareholder returns. The stronger an employee’s perception of impact on the beneficiaries of their work, the greater the employee’s motivation. Recent studies have also shown that positive social impact correlates with higher job satisfaction. Similarly, just as a sense of higher purpose can inspire employees to perform better, a weaker ESG proposition can drag productivity down via strikes, worker slowdowns, and other labor actions within the organisation.

A strong ESG proposition can enhance investment returns by allocating capital to more promising and more sustainable opportunities, such as renewables and waste reduction. It can also help companies avoid investments that may not pay off because of longer-term environmental issues, such as massive write-downs in the value of oil tankers.

Regulatory responses to emissions will likely affect energy costs and could especially affect balance sheets in carbon-intense industries. Bans or limitations on single-use plastics or diesel-fueled cars in city centers will introduce new constraints on multiple businesses. One way to get ahead of the future curve is to consider repurposing assets such as converting failing parking garages into uses with higher demand, such as residences or day-care facilities, which are a growing trend in reviving cities.

Integrating ESG into Valuation and Investment

In view of the growing importance of ESG issues and their influence on business value, investors should integrate ESG risks/opportunities and their financial impact into the valuation process and investment evaluation.

- Market based approach

A private company is usually benchmarked against comparable public companies in terms of business activities, target markets, revenue contribution and profitability. Relying on a quoted company share price and multiple to illustrate the impact of ESG actions on value is currently difficult in practice. ESG rating systems are still early stage and share prices are typically too volatile and all-encompassing to draw out the impact of individual ESG issues on the above selection criteria. To perform this analysis, there needs to be better data and better reporting standards around climate-related data for investors and valuers to make the comparison. On the bright side, with sustainability reporting becoming more prevalent and mandatory under IFRS, investors will be able to differentiate companies based on their disclosures of ESG strategy and more standardised performance metrics, and thus make informed investment decisions.

- Income approach

Valuation models may include an assessment of the most material ESG demands for key stakeholders, quantify the costs to meet or exceed them and the financial implications of doing so. Companies should assess what ESG issues are most material to their customers (e.g. it may be waste rather than carbon dioxide emissions) and benchmark the performance in these areas against competitors. Then consider price elasticity of different customers to estimate whether this will enhance or destroy brand value through changes in demand or discounted/premium pricing.

- Revenue

ESG factors can be integrated into revenue projections by increasing or decreasing the company’s sales growth rate by an amount that reflects the level of ESG opportunities or ESG risks. Take for instance, the carmakers are constantly improving their car models with the heightened awareness of ESG risks and will probably re-look into the sales.

- Operating costs and operating margin

Companies can make assumptions about the influence of ESG factors on future operating costs by either adjusting them directly or adjusting the operating profit margin. For instance, operating margin of construction companies or manufacturing companies may be reduced to reflect the high injury and fatality rates and poor health and safety standards. Similarly, the operating costs of a chemical company may increase with the additional costs associated with new legislation on toxic waste.

- Terminal cashflows

Companies should consider the long term prospects for customers in their sectors – whether they will move to greener substitute products or services that emerge, as this will affect estimates of market share and size and therefore terminal value beyond the explicit forecast period. Certain ESG risks may also trigger doubt of sustainability of business model and foreseeable closure, hence resulting in terminal value of zero.

- Adjustment to discount rate

Discount rate is typically derived from the Capital Asset Pricing Model (CAPM) with reference to a set of comparable companies to the subject company based on the best fit in terms of business activities, market capitalisation and revenue contribution. The beta or discount rate used in company valuation models may be further adjusted to reflect ESG factors: corporate governance, operational management, general quality of management, its strategic decision making etc. Companies within the sector can be analysed and ranked using ESG factors. The beta or discount rate can be increased or decreased for companies considered to possess high or low ESG risk, thus in turn reducing or increasing the overall value of the company.

Given the significant demand from investors and lenders for ESG investment opportunities, ESG performance metrics are increasingly linked to the cost of debt through the inclusion of ESG linked debt margin ratchets. Depending on the instrument (i.e. a loan or a bond) the cost of debt may increase or decrease in line with the borrower’s performance on pre-agreed ESG targets. Despite these advancements, they are rarely being factored into valuations, so assessing which ESG KPIs lenders are focusing on within the subject sector and understanding the company’s performance in these areas could have a significant impact on cost of debt and therefore value.

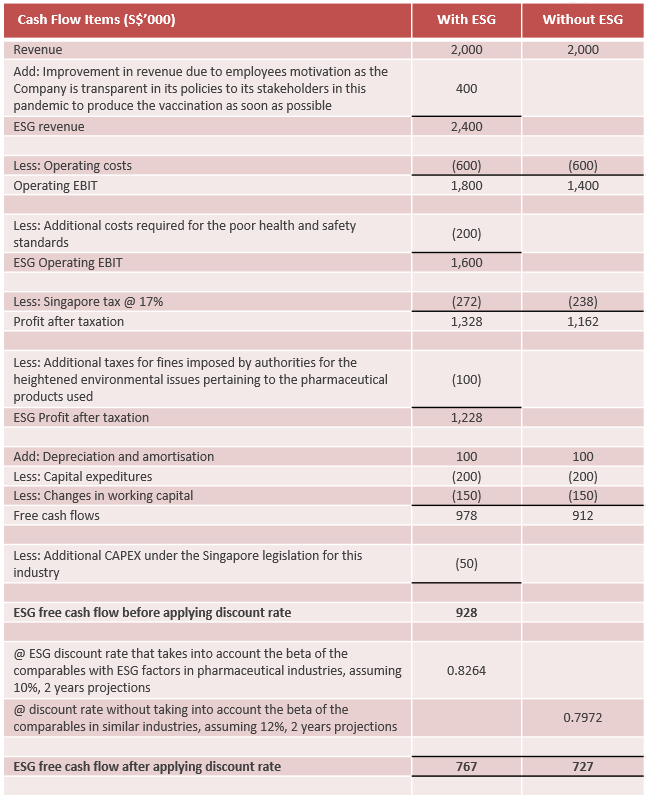

The following is an illustration of a pharmaceutical company incorporating ESG factors and the financial impact on value.

- Scenario analysis

Cash flows with material ESG factors integrated can be projected and compared against the baseline cashflows. The differences between the two scenarios will clearly depict the materiality and magnitude of ESG factors affecting a company. The inputs will be similar to what had been done during the Covid-19 pandemic period to account different recovery paths and impact of recovery.

Contact Our Specialists for A Discussion

CLA Global TS (formerly Nexia TS) has a group of professionals with the experience to bring the focus of ESG to another level for the near future.

Please feel free to contact us for a personal consultation.

Valuation Advisory Specialists

|

Grace Lui Director, Valuation & Transaction Services gracelui@sg.cla-ts.com |

|

Karen Lau Associate Director Valuation & Transaction Services karenlau@sg.cla-ts.com |

Sustainability Advisory Specialists

|

Pamela Chen Director, Head of Internal audit & Sustainability & Climate Change pamelachen@sg.cla-ts.com |

|

Krishna Sadashiv Advisor, Sustainability & Climate Change ksadashiv@sg.cla-ts.com |

|

Maria Teo Associate Director, Sustainability & Climate Change mariateo@sg.cla-ts.com |